Download PDF Version

Download PDF Version

Executive Summary

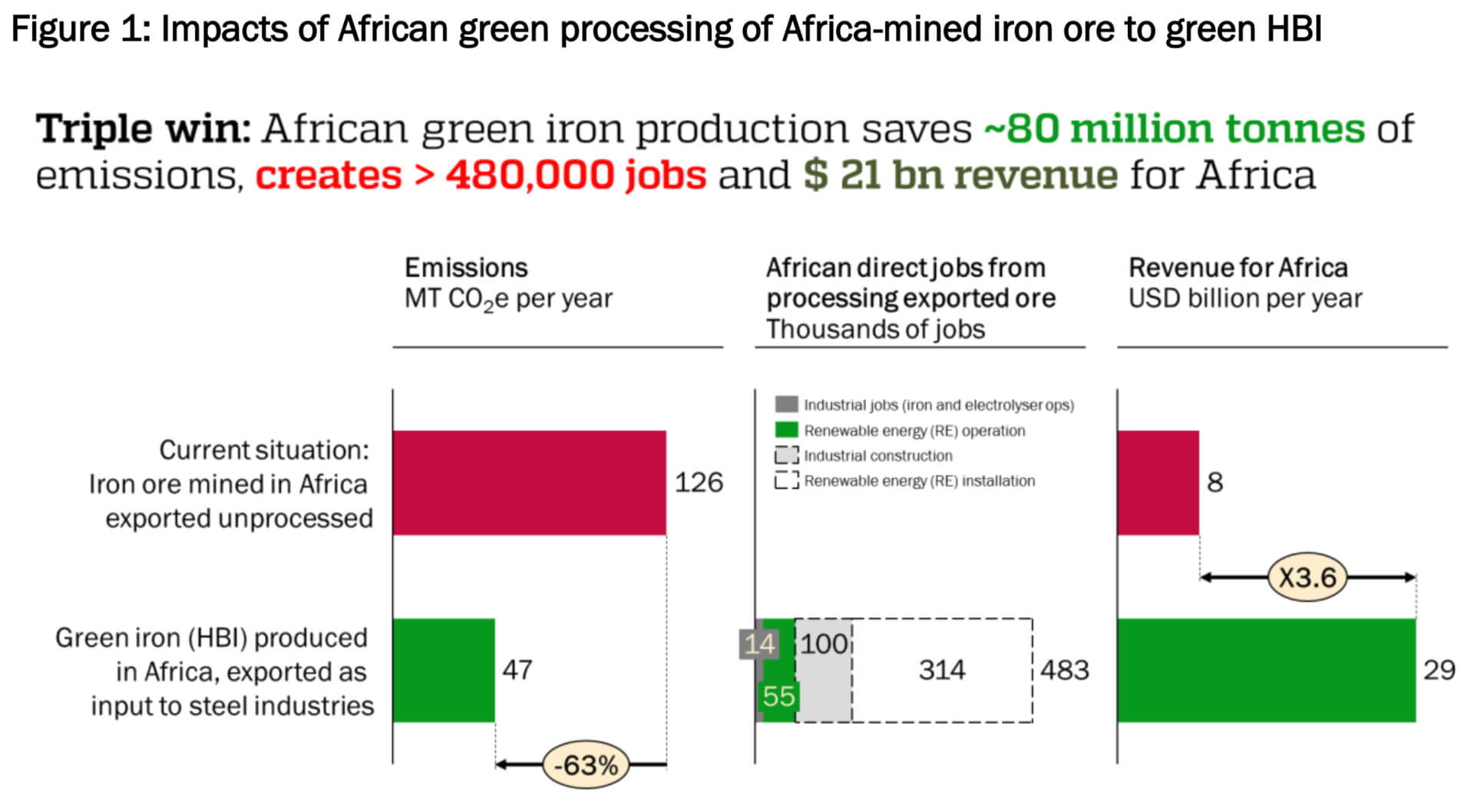

Africa’s ability to convert its iron ore into green hot briquetted iron (HBI) is emerging as one of the most consequential industrial and climate opportunities of this decade. And while mineral processing features increasingly in African industrialisation discussions, this is the first time the employment potential of green HBI has been fully scoped. Processing all African iron ore into green HBI at the mine site would generate over 480,000 jobs — including over 410,000 once-off construction jobs (quantified in job-years) and over 70,000 permanent industrial and operations roles. The majority of these jobs stems from Africa’s renewable-energy build-out and operation, underscoring the centrality of clean energy in enabling competitive green industry.

The global climate implications are equally significant. Producing green HBI in Africa cuts emissions associated with African iron ore from 126 MT to 47 MT, a 79 MT annual reduction. Nearly 70 MT of this comes from reduced emissions in China (54 MT) and Europe (15 MT) — the two largest importers of African ore — when they replace fossil-based ore processing with green HBI.

This shift also clarifies a broader global opportunity. Green HBI demonstrates the gains from allocating renewable energy across borders according to the intrinsic comparative advantage, accelerating global industrial decarbonisation. Europe is one clear example: it faces interlinked constraints — tight electricity systems, slow permitting, and structural limits on affordable green hydrogen — that make expanding energy-intensive upstream ironmaking domestically expensive and slow. Producing green HBI in Africa resolves these constraints by shifting the most energy-intensive step of steelmaking to regions with abundant, low-cost renewable energy while supplying Europe with the clean metallic inputs needed for its industrial transition and allowing it to retain strategically important steelmaking capacity.

The opportunity extends well beyond green iron. The methodology developed here provides a replicable template to assess the potential for Africa across other energy-intensive value chains. Realising this potential requires aligning trade, investment and industrial policy frameworks with this emerging global industrial structure.

1. Africa’s Industrial Opportunity: Processing at the Source

Most of Africa’s iron ore is exported in raw form, with processing taking place elsewhere, often in highly fossil-intensive systems. This prevents African economies from capturing industrial value and limits the deployment of renewable energy that could anchor competitive heavy industry.

Africa’s solar, wind and geothermal endowment is among the strongest in the world, providing Africa with the intrinsics to become globally cost-competitive in renewable generation, and thus in green hydrogen and renewable-powered reduction.

New jobs, new value, new capability

Processing all iron ore exported from Africa into green HBI would:

- Generate over 480,000 jobs, including

- over 410,000 construction job years, and

- nearly 70,000 permanent industrial and operational roles.

- Retain USD 21 billion annually on the continent.

- Reduce associated emissions from 126 MT to 47 MT, avoiding 79 MT each year.

Methodology: Estimating job opportunities

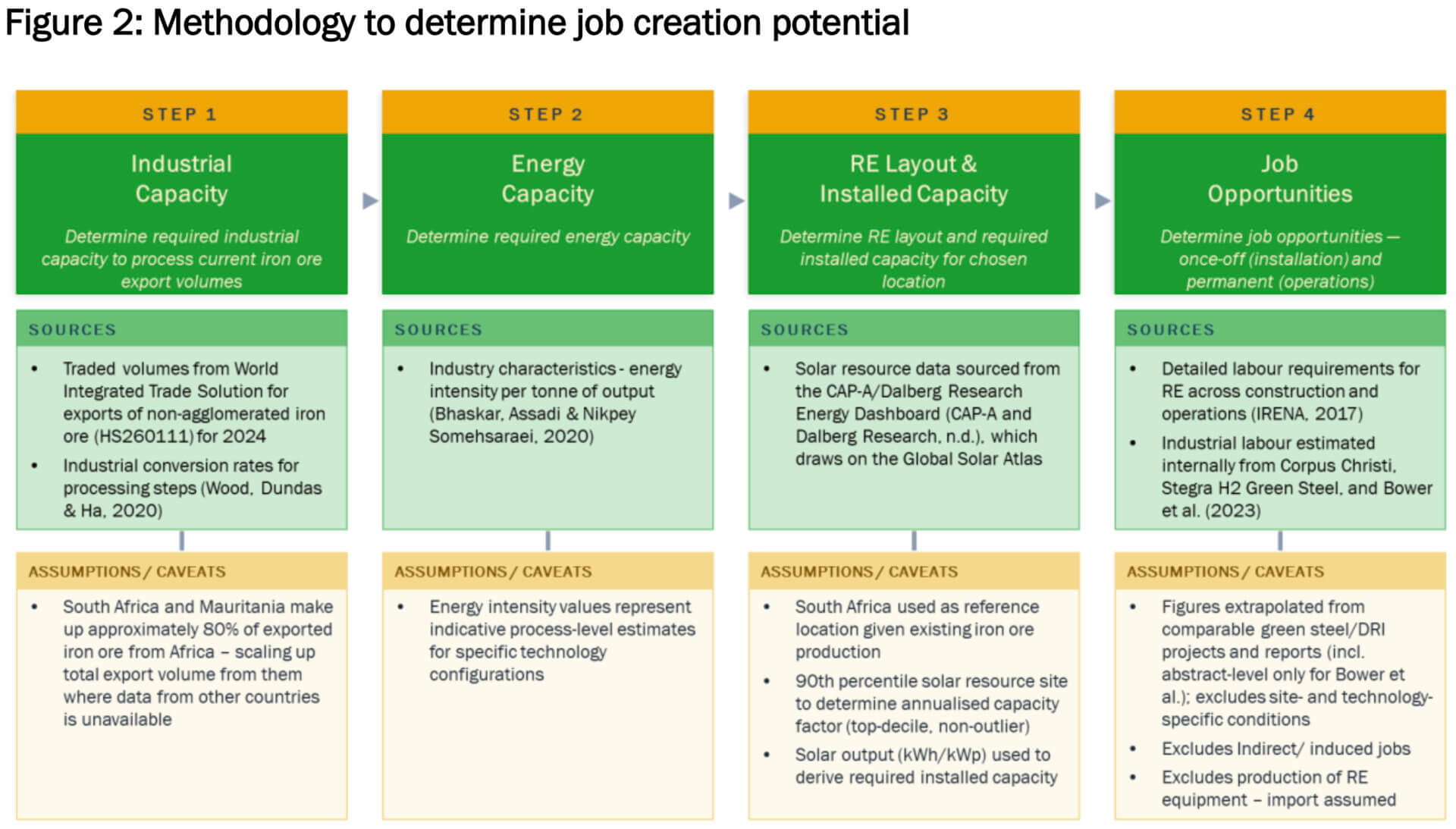

We estimated job creation by modelling the industrial and energy capacity required to process all African iron ore exports into green HBI. First, we calculated the scale of processing capacity needed using 2024 export volumes for non-agglomerated iron ore and industrial conversion rates from established green-steel studies. We then translated this capacity into energy requirements using process-level energy-intensity benchmarks for direct-reduced iron.

Next, we determined the renewable-energy build-out required to power this production. This relied on solar resource data for high-quality sites associated with existing iron-ore production regions and used top-decile capacity factors to derive indicative installed capacity needs. Job estimates for construction and operations were then produced by applying detailed labour coefficients for renewable-energy deployment alongside industrial labour estimates from comparable large-scale green steel and hydrogen projects. The results represent direct jobs only and exclude indirect or induced employment effects. Figure 2 provides further detail on the methodology and includes assumptions. A bibliography of sources can be found in the Annex.

2. Global Climate Impact: 79 MT of Emissions Reduced —Driven by China and Europe

Shifting iron-ore processing to Africa and powering it with renewable energy cuts global emissions associated with African iron ore from 126 MT to 47 MT — a 79 MT annual reduction. This is one of the single largest decarbonisation levers available in the global iron and steel system today.

Within this total global reduction, two regions drive the majority of the impact:

China: 54 MT of emissions reduced annually

China is the dominant destination for African iron ore. Its current steel production remains heavily coal-dependent, particularly in the upstream reduction stage. When African iron ore arrives as green HBI instead of raw ore, China avoids 54 MT of emissions every year. This represents the largest share of the global climate benefit delivered by African green HBI.

Europe: 15 MT of emissions reduced annually

Europe is a smaller importer of African iron ore but still a significant contributor to global impact. Replacing fossil-based processing with African green HBI avoids 15 MT of emissions annually for the volumes Europe currently imports. It also supports Europe’s transition to cleaner EAF-based steelmaking without putting additional pressure on its already constrained power systems.

Taken together

China and Europe account for nearly 70 MT of the 79 MT global reduction, underscoring the central role of African green HBI in decarbonising the world’s two largest steel markets. This reduction potential excludes any further greening of the power grid for downstream Electric Arc Furnace steel-making. As this greening is happening, the total associated emission reductions will only grow.

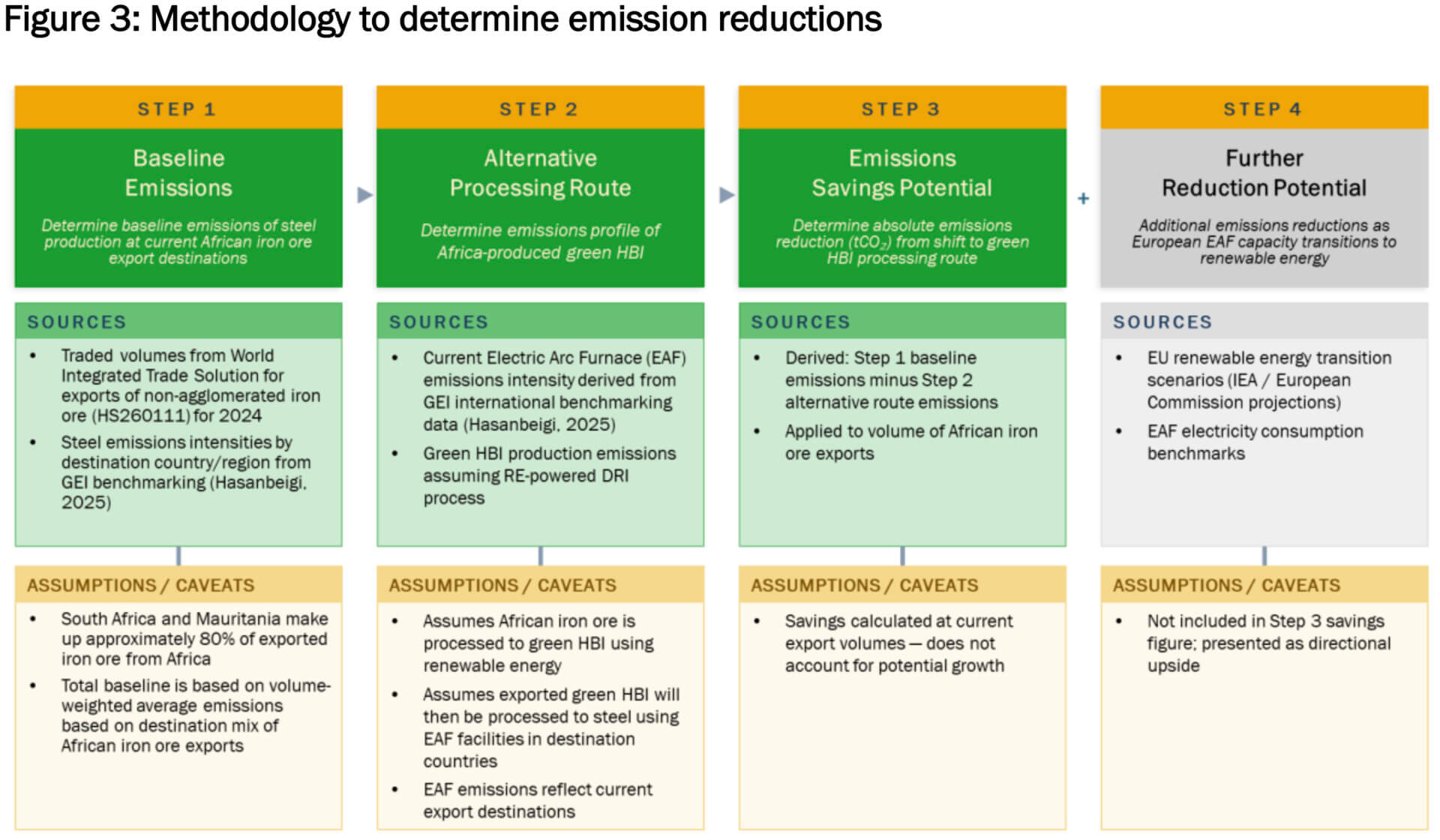

Methodology: Estimating emissions reductions

Baseline emissions were calculated by assessing current destination-country emissions associated with African iron-ore exports. This baseline reflects prevailing industry practice and therefore assumes that exported ore is processed into crude steel through integrated Blast Furnace–Basic Oxygen Furnace (BF-BOF) routes. We combined 2024 export volumes with destination-specific steel emissions intensities from international benchmarking data to determine baseline emissions.

We then modelled the alternative pathway in which African iron ore is processed into green HBI using renewable energy and subsequently converted to steel in Electric Arc Furnaces (EAFs) in destination markets. The emissions intensity of this route was derived from current EAF benchmarks combined with assumptions of renewable-powered DRI in Africa. Emissions reductions equal the difference between the baseline BF-BOF pathway and the green HBI– to-EAF pathway, applied to current export volumes. Potential further reductions from fully renewable-powered EAFs in Europe were noted as additional upside but excluded from the headline savings figure. Figure 3 includes further detail and assumptions, with sources detailed in the Annex.

3. How Green HBI Helps Europe Resolve Its Interlinked Decarbonisation Constraints

Europe’s steel transition is constrained by interlinked system challenges: electricity scarcity, slow permitting, and structural limits on scaling affordable green hydrogen. These constraints are not discrete — they are interconnected and compound one another. Green HBI addresses them directly.

Europe’s electricity system is tight —and every megawatt has an opportunity cost

Electrification of transport, buildings and data-intensive industries is accelerating. But renewable expansion is slowed by permitting timelines, land availability, and grid bottlenecks. This creates structural scarcity.

In this context, allocating huge volumes of renewable electricity to upstream iron reduction — one of the most energy-intensive industrial steps — carries high opportunity costs. Hydrogen-based reduction competes with direct electrification of heating, mobility and large industrial loads.

Green hydrogen is constrained by the same system friction

Electrolysers need large volumes of stable, low-cost renewable electricity. Europe cannot provide this at scale fast enough. Importing hydrogen over long distances is also not the solution: liquefaction, ammonia conversion or use of carriers adds energy losses and cost premiums that undermine its role in large-volume industrial decarbonisation.

Green HBI solves this system -level problem

Green HBI embodies the clean energy needed for iron reduction in a stable, tradable form. It shifts the most energy-intensive stage of steelmaking to regions with abundant, low-cost renewables — such as Africa — while allowing Europe to:

- Free domestic renewable capacity for higher-value uses;

- Accelerate the shift to EAF-based steelmaking;

- Reduce emissions by 15 MT annually without expanding energy-intensive upstream capacity.

Green HBI is therefore not only a commodity but a system solution: it reconciles Europe’s industrial decarbonisation goals with its structural energy constraints.

4. Why This Matters —and What It Takes to Get This Right

The green HBI opportunity shows that climate-aligned industrialisation can be a source of strategic resilience, not a constraint. But realising this potential at scale is not automatic. It depends on whether trade, investment and industrial policy frameworks evolve to reflect this emerging global industrial structure. It also requires a very significant expansion of Africa’s generation capacity, much of it likely renewable, which will influence project design and regulatory planning.

Getting this right requires four shifts:

- Align measures with emissions performance, not location. Standards, incentives and border measures should recognise and reward verifiable low-emissions products, regardless of where the energy-intensive processing takes place.

- Design trade and investment rules for integrated value chains. Financing tools, trade agreements and industrial strategies need to treat African green HBI as a core input to Europe’s industrial transition, not as a residual import.

- Translate policy intent into bankable projects. Long-term offtake arrangements, risk-sharing instruments and clear eligibility rules are needed to crowd in investment on both sides of the Mediterranean and support large-scale HBI projects anchored in African renewables.

- Integrate energy system design into industrial strategy. African countries face a large new build-out rather than a transition from legacy fossil systems. Designing this expansion around renewable generation for energy-intensive industry allows for step-changes in capacity while addressing persistent energy deficits. Doing so requires coordinated planning for storage, load balancing and grid management from the outset.

Proposed EU legislation such as the Industrial Accelerator Act will be pivotal. If designed narrowly around domestic-first production — for example by tying support to locally produced hydrogen or upstream processing — such measures risk making Africa–EU industrial collaboration harder, not easier. They could misalign incentives, crowd capital into higher-cost domestic options and limit Europe’s access to low-emissions HBI from Africa.

It matters a great deal: Africa’s renewable advantage can underpin a new, globally efficient industrial structure. Europe secures a credible, lower-cost decarbonisation path. China can accelerate steel decarbonisation without waiting for full domestic hydrogen build-out. And Africa realises jobs, revenue and industrial capability at the core of its growth model.

5. Applying This Methodology to Future Industrial Opportunities

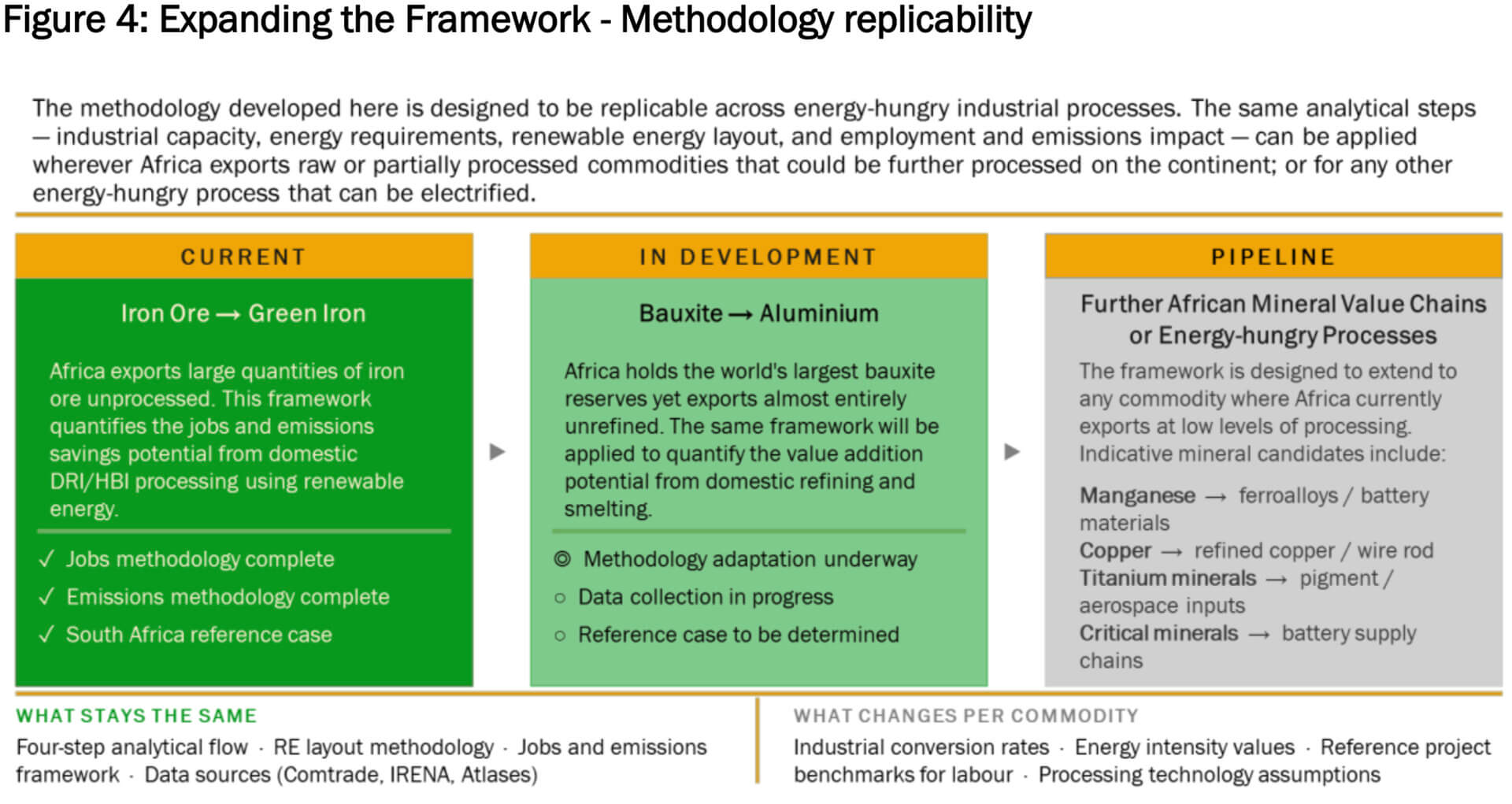

The methodological approach developed for green HBI provides a replicable way to assess the benefits of different options for green industrial focus for Africa in energy-intensive industries. It is designed for any process for which competitiveness is fundamentally shaped by access to abundant, reliable and low-cost renewable energy — including solar, wind, geothermal and hybrid configurations. These are the processes where Africa’s energy endowment, land availability and industrial expansion potential combine to offer a distinct strategic edge.

By quantifying baseline production routes, modelling renewable-anchored alternatives, and estimating job creation, economic value, and emissions outcomes, this methodology enables evidence-based prioritisation of Africa’s green industrial opportunities. Job creation is central: high-energy processes require large construction and operational workforces when combined with renewable-energy deployment. Economic value — through retained earnings and upgraded exports — provides a complementary and distinct benefit.

This approach is already being applied to bauxite refining and aluminium production, among the world’s most electricity-intensive industrial processes. Early work indicates similar dual advantages: substantial job creation and significant global emissions reductions when these processes are shifted from fossil-constrained regions to Africa’s renewable-rich locations. Further applications may include green fertilisers, cement substitutes, battery precursor materials and green chemicals.

Used consistently, this methodology becomes a strategic tool for governments, financiers and investors to determine where Africa can prioritise green industrial development based on the climate, revenue, and job creation benefits each option can realise. A visual summary of this replicability framework is captured in the slide below.

Download PDF Version

Annex: References and Sources

The following references constitute all sources cited in the two methodology slides (Figures 2 and 3) that underpin the analytical approach used in this report. Please note that labour intensity is an area of much uncertainty. We explored many sources across reported projects, surveys, and academic (including partially modelled) sources. Upon request, we can provide further detail on sources considered and rationale for using the IRENA/ ILO source. As data and insights evolve further, we will adjust the inputs accordingly.

ArcelorMittal. (2022, Apazasril 14). ArcelorMittal acquires majority stake in voestalpine’s state-of-the-art HBI facility in Texas [Press release]. https://corporate.arcelormittal.com/media/press-releases/arcelormittal-acquires-majoritystake-in-voestalpine-s-state-of-the-art-hbi-facility-in-texas (Accessed: February 2026).

Bhaskar, A., Assadi, M., & Nikpey Somehsaraei, H. (2020). Decarbonization of the iron and steel industry with direct reduction of iron ore with green hydrogen. Energies, 13(3), 758. https://doi.org/10.3390/en13030758 (Accessed: February 2026).

Bower, G., Jones, W., King, B., & Pastorek, N. (2023). Clean hydrogen workforce development: Opportunities by occupation. Rhodium Group. https://rhg.com/research/clean-hydrogen-workforce-development/ (Accessed: February 2026).

Climate, Infrastructure and Environment Executive Agency (CINEA). (n.d.). Stegra: Welcoming a new era of green steel production. Featured Projects. https://cinea.ec.europa.eu/featured-projects/stegra-welcoming-new-era-green-steelproduction_en (Accessed: February 2026). Corroborated by Midrex Technologies project disclosures; Boden municipality employment Q&A (October 2024); AFP/Sun-Commercial construction site workforce report (November 2025).

Climate Action Platform Africa (CAP-A) & Dalberg Research. (n.d.). Energy Dashboard: Solar and Wind. https://gisresearch.dalbergresearch.com/cap-a_energydashboard/ (Accessed: February 2026). Dashboard draws on the Global Solar Atlas and Global Wind Atlas.

Hasanbeigi, A. (2025). Steel climate impact 2025: An international benchmarking of energy and GHG intensities. Global Efficiency Intelligence. https://www.globalefficiencyintel.com/s/Steel-benchmarking-10102025-E1.pdf (Accessed: February 2026).

International Renewable Energy Agency (IRENA). (2017). Renewable energy benefits: Leveraging local capacity for solar PV. IRENA. https://www.irena.org/- /media/Files/IRENA/Agency/Publication/2017/Jun/IRENA_Leveraging_for_Solar_PV_201 7.pdf (Accessed: February 2026).

Wood, T., Dundas, G., & Ha, J. (2020). Start with steel: A practical plan to support carbon workers and cut emissions. Grattan Institute. https://grattan.edu.au/wpcontent/uploads/2020/05/2020-06-Start-with-steel. (Accessed: February 2026).

World Bank. (2024). World Integrated Trade Solution (WITS): UN Comtrade trade data. Trade statistics for iron ores and concentrates (HS 2601). https://wits.worldbank.org/trade/comtrade/ (Accessed: February 2026)

About CAP -A

Climate Action Platform – Africa (CAP-A) exists to demonstrate how Africa can achieve inclusive economic growth through climate-action – a focus we call Climate Positive Growth. CAP-A’s work starts from a simple premise: Africa’s structural advantages in untapped renewable energy potential, young and entrepreneurial workforce, and relevant natural assets and resources make it one of the most competitive regions globally for climate action across green industrialisation and manufacturing, climate-smart agriculture, nature protection and carbon removal.

Africa’s unparallelled untapped solar, wind, geothermal and land availability, paired with the continent’s rapidly growing workforce and abundant mineral endowment, and relatively limited existing industrial infrastructure that needs to be dismantled or transitioned away from, positions Africa to lead in the next wave of global green industry.

CAP-A translates this potential into action by generating rigorous, sector- and country-specific evidence on where Africa can compete in low-carbon production. This includes quantifying job creation, assessing renewable-energy requirements, mapping global supply-chain dynamics and identifying opportunities where African production can deliver lower emissions and lower costs than incumbent systems. The green HBI opportunity presented in this report is one such case: a combination of potential for industrial competitiveness, system-level decarbonisation, and large-scale employment anchored in renewable-energy deployment.

Beyond analytics, CAP-A works directly with governments, investors, industrial actors and global rule-shapers to align policy, financing and market access with Africa’s emerging industrial advantage. This includes supporting the conceptualisation of bankable industrial projects, informing trade and industrial policy, building proof-of-concept demonstrations and ensuring African priorities are reflected in global market frameworks. Across all of its work, CAP-A connects economic development and climate ambition, showing that climate-aligned industrialisation is not a trade-off but a pathway to long-term competitiveness, job growth, and inclusive development.

CAP-A Co-Founder Carlijn Nouwen is the lead author for this report. CAP-A staff Matthew Hill and Caris Zwane provided much of the analytical work, along with Dr Jasper Grosskurth and his team at LOCAN/ DR.

Please contact us at [email protected] if you have any questions, comments, or suggestions. We look forward to hearing from and partnering with you.

]]>