Did you find this article useful?

Subscribe to the HOT|COOL newsletters for free and get insightful articles on a variety of topics delivered to your inbox twice a month!

The post UKRAINIAN DELEGATION LOOKS TO DENMARK FOR RESILIENT, FOSSIL-FREE HEAT SOLUTIONS first appeared on DBDH.

]]>That was the starting point when a Ukrainian delegation of district heating decision-makers visited Denmark from 17–19 March for a three-day program focused on modernization, green transition, and long-term recovery. Organized by DBDH in cooperation with the Royal Danish Embassy in Ukraine, the visit brought together 16 representatives from Ukrainian municipalities and district heating companies.

The delegation met Danish stakeholders in Copenhagen before continuing to site visits on Zealand and Funen. The aim was clear: to connect Ukrainian recovery needs with Danish experience in district heating, energy efficiency, and integrated heat planning.

Ukraine’s district heating sector is one of the largest in Europe, supplying heat to more than 100 cities and over 100,000 buildings. But the sector is under severe pressure. War damage, worn-out infrastructure, and a historic reliance on natural gas have made the need for modern, reliable, and more sustainable heat solutions urgent.

For that reason, the Danish site visits were more than technical showcases. They were practical examples of how heat systems can be planned and operated with flexibility, integration, and long-term resilience in mind. The program included visits to utilities such as Frederiksberg Forsyning, Høje Taastrup Fjernvarme, ARGO, Sorø Fjernvarme, Assens Fjernvarme, and Envafors.

As DBDH puts it: “The site visits show good examples of how local Danish district heating companies can play an important role as knowledge-sharing partners. It is exactly this practical experience that international delegations come to Denmark to see and learn from.”

At Envafors, the delegation was introduced to the practical realities of local heat supply, operations, and knowledge sharing.

Henrik Birch, CEO of Envafors, says:

“We are pleased to share our experience with district heating and show how a Danish utility can help create a more stable and sustainable local heat supply. At Envafors, we have gained extensive practical experience — not only with the technology itself, but also with cooperation and knowledge sharing. That combination is exactly what makes district heating an important part of the solution when cities want to strengthen energy security while reducing their climate footprint.”

At Assens Fjernvarme, the conversation added another dimension: district heating as critical infrastructure. Here, the dialogue focused not only on decarbonization, but also on preparedness and the need to operate under increasingly uncertain conditions.

Marc Roar Hintze, Director of Assens Fjernvarme, says:

“We see this as an opportunity to learn from each other. In Denmark, we talk about district heating as critical infrastructure — but our Ukrainian colleagues are working under truly extraordinary conditions, which puts that into a very different perspective.”

He also points to a lesson that reaches beyond Ukraine: “The ability to operate critical infrastructure independently of the wider system is no longer a theoretical scenario — it is a real challenge that should also be reflected in future political priorities.”

That message resonated strongly during the visit. Ukraine’s recovery is not only about replacing damaged assets. It is also about building heat systems that are more flexible, less dependent on fossil fuels, and better prepared for future disruption. Denmark’s district heating sector cannot solve that challenge alone, but it can offer something highly valuable: proven solutions and practical experience.

For DBDH, that is exactly the point. When Danish utilities open their doors to international delegations, they do more than share knowledge. They show how modern heat supply works in practice — and how local experience can support broader international partnerships.

Curious to learn more?

Curious to learn more?Read the latest industry news on dbdh.org here.

The post UKRAINIAN DELEGATION LOOKS TO DENMARK FOR RESILIENT, FOSSIL-FREE HEAT SOLUTIONS first appeared on DBDH.

]]>The post Karen Grønning Mikkelsen first appeared on DBDH.

]]>

The post Karen Grønning Mikkelsen first appeared on DBDH.

]]>The post THE MARCH EDITION OF HOT|COOL IS OUT first appeared on DBDH.

]]>The post THE MARCH EDITION OF HOT|COOL IS OUT first appeared on DBDH.

]]>The post FLEXIBILITY BY ELECTRIFICATION OF DISTRICT HEATING first appeared on DBDH.

]]>By Shervin Balali, Expert Renewable Heat, Dr. Jana Bosse, Senior Expert for Renewable Heat, Dr. Rita Ehrig, Team Leader for Renewable Heat, and Dr. Tim Mennel, Lead Expert for Market Design, German Energy Agency (dena)

Published in Hot Cool, edition no. 2/2026 | ISSN 0904 9681 |

The analysis presented in this article is based on a literature review of publicly available studies and reports, as well as eleven structured interviews with Danish and German industry experts. Participants included professionals from district heating companies, transmission system operators, and researchers.

While Denmark and Germany both strive to electrify their heating network supply, they are currently at different stages of development. Denmark already meets a notable share of its heat demand through power-to-heat technologies, harnessing their flexibility to support the electricity system. In contrast, German district heating providers currently use very little power-to-heat appliances, with plans to expand their use in the future. In that respect, Germany resembles other European nations seeking to decarbonise their district heating systems.

For district heating operators, electrification is not only a path to decarbonization but also offers new revenue opportunities through participation in the electricity market by providing flexibility. District heating can provide flexibility, for example, through system-friendly geographical relocation of heat generation and the provision of ancillary services. At the same time, participation in wholesale and ancillary service markets can improve the techno-economic performance of heat-generation assets and strengthen the business case for electrified heating technologies overall.

The electricity grid has no storage capacity. Supply and demand must thus be constantly balanced, or, in technical terms, the frequency of the European interconnected alternating current grids must be equal to, or close to, 50 hertz. To ensure network stability, network operators procure so-called ancillary services from participants in the electricity markets [1].

The procurement of ancillary services is organised along grid zones rather than bidding zones. Western Denmark and Germany are both part of the Continental European System Area (CESA), one of the largest synchronous electrical grids in the world [1]. Most of the regulations and requirements are therefore identical, although there are some differences in national implementation. Overall, the following ancillary services are available for frequency control (also called balancing services) in this control area: frequency control reserve (FCR), automatic frequency restoration reserve (aFRR), and manual frequency restoration reserve (mFRR). The services differ in terms of the activation timeline; see Figure 1.

Figure 1: Balancing services in CESA (own illustration based on Nextkraftwerke, 2025 [2])

In the past, thermal electricity plants provided the bulk of ancillary services; in particular, gas turbines with their high reactivity are technically suitable for frequency control and other ancillary services. Moreover, pumped hydro storage plants contribute to the supply of ancillary services, in particular frequency control. When the expansion of renewable generation began in the 2000s, some observers feared that the fluctuations in wind and solar generation would necessitate vast frequency-control capacity.

Today, it is clear that the warnings were exaggerated. The introduction of intraday markets alleviated the negative effects of fluctuations on the scheduling of generation assets. However, the phase-out of thermal generation at a more advanced stage of the electricity system’s transition creates a need for new suppliers of ancillary services, particularly in systems without (or with only small shares of) hydropower. Some ancillary services can indeed be provided by renewable assets themselves, many others by batteries and by demand response technologies.

It must be emphasised that the use of flexible assets in the electricity system does not end here. Flexible demand (as well as storage) can and is marketed in the spot market. Here, it helps accommodate fluctuating electricity feed-in, allowing for a match of demand and volatile supply via arbitrage. In terms of volume, the spot market is, of course, much more important than the frequency control market: the financial trading volume in the German day-ahead market is around 30 times higher than that of the balancing market.

In Germany, the list of prequalified capacity for frequency control services shows a clear picture: pumped hydro storage leads by a wide margin across FCR, aFRR, and mFRR. Battery storage comes next for FCR, while natural gas plants rank second for aFRR and mFRR. However, this snapshot no longer reflects actual market behaviour. Today, batteries deliver around 95% of FCR.

There has been a sharp rise in new battery storage, mainly due to price advantages linked to temporary exemptions from grid fees. A look at Denmark tells a different story, with prequalified FCR capacity being largely dominated by electric boilers and batteries. Regarding aFRR and mFRR, again, electric boilers play a major role for both up- and down-regulation, followed by wind turbines and conventional plants. Figure 2 summarises the prequalified assets for FCR in Germany and (Western) Denmark.

The post FLEXIBILITY BY ELECTRIFICATION OF DISTRICT HEATING first appeared on DBDH.

]]>The post FLEXIBILITY IS NOT OPTIONAL – IT IS THE NEW FOUNDATION OF DISTRICT HEATING first appeared on DBDH.

]]>

The post FLEXIBILITY IS NOT OPTIONAL – IT IS THE NEW FOUNDATION OF DISTRICT HEATING first appeared on DBDH.

]]>The post DEEP GEOTHERMAL ENERGY FOR DIRECT USE IN DISTRICT HEATING first appeared on DBDH.

]]>By Kim Gunn Maver, Camille Hanna, Mads Sylvest Eegholm, and Nikolaj Holmer Nissen, Green Therma

Published in Hot Cool, edition no. 2/2026 | ISSN 0904 9681 |

The new solution almost eliminates heat loss from the returning fluid to the surface and will thereby overcome the currently perceived limitations of single-well coaxial solutions. Furthermore, it increases the heat-harvesting area by adding a long horizontal section, as is common in oil and gas wells.

The solution can play a significant role in the European energy transition and deliver heat directly to the growing district heating grid without the use of heat pumps. As a result, district heating can be largely decoupled from the electricity grid, with a Coefficient Of Performance (COP) of 30-50 and a very limited surface footprint.

Green Therma and its partners have received an €11.5 million grant from the Danish Energy Technology Development and Demonstration Programme (EUDP). The grant will support the full-scale demonstration project, including a 7 km well to be drilled in late 2026. The well will supply geothermal heat directly to Aalborg Forsyning’s district heating customers under a 30-year heat-offtake agreement. The project supports the wider goal of scaling multi-well closed-loop solutions in the global energy mix.

Conventional geothermal systems are based on a doublet design, where one well produces formation water and another well injects/returns cooled formation water. The system is highly dependent on the thickness of the geological formation and the formation parameters, such as porosity, permeability, and geochemistry, to ensure hydraulic connectivity between the wells to maintain water production.

Produced water can cause corrosion, scaling, clogging, and significant maintenance issues in surface installations, the injection well, and the reservoir around the injection wellbore. Hydraulic fracking may be required to improve injectivity and formation connectivity, with the risk of polluting groundwater aquifers, having a detrimental impact on the geological formation, inducing seismicity, and potentially damaging surface infrastructure.

Because these risks can only be partially mitigated by gathering geophysical and geological data for well planning, the financial viability of a project is highly variable and unpredictable.

To mitigate issues with a doublet hydrothermal solution, a patented vacuum-insulated inner pipe circulates a working fluid in a closed-loop well. The working fluid is heated by the surrounding geological formations along a long horizontal section (Figure 1).

The working fluid, similar to the fluid in district heating pipes, flows downward between the well casing and an outer pipe, absorbing heat from the geological formations along the way, especially in the horizontal section. Once heated, the working fluid returns to the surface through a vacuumized pipe-in-pipe assembly, which consists of an inner and an outer pipe working similarly to a thermos flask.

Figure 1: Closed-loop horizontal geothermal well solution.

The continuous and controlled vacuum in the pipe-in-pipe provides thermal insulation, minimizing heat loss (Figure 2). As a result, the temperature of the fluid returning to the surface is reduced to only a few percent. Without a vacuum to insulate the circulating fluid, significant heat loss occurs.

The closed-loop solution is flexible in its heat provision. This is beneficial in cases where heat demand varies seasonally. Flexibility is achieved by either adjusting the flow rate or stopping fluid flow for a period. This allows the subsurface to reheat during under-utilized periods.

In some cases, the flow of the working fluid in the well can sustain itself by the thermosiphon effect due to the heated fluid in the inner pipe being less dense than the cold water in the outer pipe. However, fluid circulation at various flow rates requires a small circulation pump.

Figure 2: Vacuumized pipe-in-pipe solution.

There are several benefits of the closed-loop solution in general, and when compared to the conventional doublet hydrothermal solution.

The solution is largely independent of geology, meaning wells can be drilled in most locations to depths where subsurface temperatures are high enough to deliver heat without heat pumps. That also means that there is no exploration risk – a well will always produce heat.

As the general electricity requirement is only for a 45 kW circulation pump, the solution has a COP of between 30 and 50, depending on the thermal output of the well, minimizing the burden on the electrical grid.

With a very high COP, this solution has minimal CO2 emissions, and the heat pump’s electricity demand could easily be met by a green source.

In a closed-loop system, no fluids circulate within the geological layers, leaving the geology undisturbed. No downhole equipment is required; the circulation pump and surface equipment are based at surface level, gathered in an easily accessible 20-foot container. The operating cost is therefore limited to maintenance. The 20-foot topside facility can be placed below a parking lot or field, requiring only a 50 m by 50 m area around the well. The landscape footprint is therefore minimal. In addition, the initial water requirement is minimal.

With the right design, there will be no tear, wear, and corrosion, which is why the solution should work for more than 50 years.

To further develop the closed-loop solution, the technology is currently being advanced through ongoing demonstration projects.

In late 2024, the vacuumized pipe-in-pipe solution was installed at the Ullrigg test site in Stavanger, Norway, and 525 m of pipe was tested. The solution was run to the planned depth for testing the equipment design, measurements, and procedures. The insulation effect and the pipe-in-pipe design were successfully tested for further development.

A full installation began in the second half of 2025, with the first heat produced in mid 2026 at Groß Schönebeck, 50 km north of Berlin, Germany.

The Groß Schönebeck site serves to investigate the sustainable provision of geothermal energy from two deep wells completed as an Enhanced Geothermal System (EGS) and is managed by GFZ Helmholtz-Zentrum für Geoforschung in Potsdam.

The GrSk 4/05 well was drilled in 2006 to extract thermal water and to form a doublet system of hydraulically connected boreholes, with a measured temperature of 145°C at 4.4 km. However, high flow rates could not be sustained, and the well is currently suspended.

In late summer 2025, the well’s dimensions and structural integrity were tested and confirmed to be suitable for recompletion. The lowest part of the well, with the perforated section used initially to flow water, will be isolated to create a closed-loop space before installing the closed-loop well completion.

The vacuumized pipe-in-pipe system, consisting of a 3.5-inch inner pipe and a 4.5-inch outer pipe, will be installed to maintain a continuous vacuum from the surface to a depth of 3.2 km. The geothermal performance of the well, specifically the transfer of heat from the geological formations, will be tested to assess the effects of varying flow rates. The average modelled output is 0.4 MW.

The overall performance of the formation’s heat transfer and the vacuumized pipe-in-pipe solution will be evaluated over a one-year period. The geothermal performance test of the solution will further qualify the completion tubing design and structural modelling for circulating varying fluid temperatures in the well.

In a collaboration between Aalborg Forsyning and Green Therma — and project partners also including Aarhus University, Aalborg University, Danish and Greenland Geological Survey, and Energy Cluster Denmark — a geothermal demonstration plant will be built in Storvorde. Green Therma will operate the facility and deliver heat for the next 30 years through a heat offtake agreement with Aalborg Forsyning (Figure 3). The project is supported by the Danish Energy Technology Development and Demonstration Programme (EUDP) with 11.5 mill Euro.

In late 2026, the geothermal well with a slanted section will be drilled, and the vacuumized pipe-in-pipe solution will be installed. The well will deliver geothermal heat directly without heat pumps to the city’s district heating network starting in 2027 (Figure 4).

Figure 3: Storvorde well location

The Storvorde location was chosen for its favourable underground geological conditions and proximity to the existing district heating network. These two factors are crucial for the plant to be established. When the plant is completed, it does not take up much space on the surface.

Prior to drilling the well, a 2-dimensional seismic survey of the subsurface will be conducted by trucks driving along roads in the area around Storvorde, emitting a pressure wave into the ground and recording the response. The seismic acquisition results in a better understanding of the local geology, enabling optimization of the final well design.

The total well length is 7 km: 4–5 km vertically, followed by a 2–3 km horizontal section. The vacuumized pipe-in-pipe solution, consisting of a 4.0-inch inner pipe and a 5.5-inch outer pipe, will be installed to maintain a continuous vacuum from the surface to 7 km.

With a geothermal temperature increase of roughly 30°C per km, a virgin temperature of 120–150°C is predicted, with a long-term minimum of 80°C at the surface for more than 50 years, while the return temperature from the district heating grid after heat exchange will be around 40°C. The only energy demand is a 45 kW for a circulation pump for <2 MW well.

Figure 4: Schematic subsurface model.

Previously, the economics of coaxial closed-loop geothermal solutions has been questioned because they cannot produce sufficient geothermal heat at a competitive price. This issue is addressed through reduced heat loss from the vacuumized pipe-in-pipe solution, the long lateral well section increasing the heat uptake area, and industrialization of the geothermal drilling process.

A long horizontal section to harvest heat is a best practice and an improved well design, especially from the USA onshore unconventional oil and gas industry. The designs have demonstrated the ability to drive the major production increase in oil and gas production since 2010, and horizontal wells have become the predominant method when drilling for oil and gas in the USA, with more than 75% of all newly drilled wells having a horizontal section.

In a 2024 International Energy Agency report, it was estimated that 80% of the investment required in a geothermal project involves capacity and skills that are common in the oil and gas industry. Furthermore, it was estimated that with the engagement from policymakers and the oil and gas industry, the costs for next-generation geothermal wells could decrease by up to 80% by 2035.

While the operations in Aalborg involve a single well, the plan for future projects is to take a “multi-well” approach across global sites, drilling a sequence of 5–10 wells from a single surface location, each with horizontal sections extending in different directions (Figure 5). This approach will reduce costs per well by minimizing rig mobilization expenses and leveraging drilling efficiency through repetition.

Figure 5: Example of a 5-well closed-loop geothermal well design.

For further information, please contact: Kim Gunn Maver, at [email protected]

The post DEEP GEOTHERMAL ENERGY FOR DIRECT USE IN DISTRICT HEATING first appeared on DBDH.

]]>The post From Billing Tools to Network Brains: UNLOCKING THE HIDDEN VALUE IN YOUR HEAT METERS first appeared on DBDH.

]]>By Peter Friis Østergaard, Senior Specialist & Thomas Schrøder Daugbjerg, Consultant, Danish Technological Institute

Published in Hot Cool, edition no. 2/2026 | ISSN 0904 9681 |

Simultaneously, traditional energy meters at the consumer, used solely for billing, have been replaced by remotely read “smart meters” that provide hourly data. Apart from providing valuable insights into consumption patterns and network loads, enabling better forecasting and operational planning, these meters also enable utilities to offer motivational tariffs based on, e.g., absolute return temperatures.

However, a fundamental limitation remains: these meters are built as billing devices, not high-precision laboratory instruments. Their data, while useful, is not intended to serve as precise, absolute measurements, which complicates fine-grained analysis of the network’s physical health. But what if these meters could become the key to a smarter, safer, and even more cost-effective network?

What if, instead of acting as isolated billing devices with insufficient data quality for advanced system optimization, your meter could operate as part of a network of intelligent sensors? By co-calibrating, they allow you to pinpoint exactly which pipes are losing the most heat and which meters are drifting toward inaccuracy. [LB1.1]

Advanced analyses have demonstrated the ability to accurately estimate the energy meter’s temperature offset with precision below 0.5 °C and the insulation level of service pipes with precision down to 0.01 W/m/K, all in real time, enabling fast responses from utilities when required. Knowing these values with high precision allows for utilities to focus their maintenance at places where they have the highest impact with significant potential savings as a result.

Figure 1: Data from remotely ready meters should be analyzed based on the physical network in which they are located. Including neighbouring meters in an analysis improves the potential value manyfold, as correlations between meters and the physical network can be exploited.

Figure 1: Data from remotely ready meters should be analyzed based on the physical network in which they are located. Including neighbouring meters in an analysis improves the potential value manyfold, as correlations between meters and the physical network can be exploited.

District heating meters are designed to measure energy consumption by tracking water flow and the temperature difference between the supply and return pipes. They are factory-calibrated for this specific purpose. Since the temperature sensors in an energy meter are placed in roughly the same environment throughout their lifetimes, it can be expected, from a physical standpoint, that they will age identically. As such, their temperature difference measurement will remain stable, while the absolute temperature reading can develop an offset over time.

While meters are factory-calibrated and must meet standards before installation, their long-term stability is rarely verified. Utilities must perform spot checks on a small sample from a batch, but most sensors are left unmonitored unless an obvious error occurs. On top of this, sensor couples can get damaged by accidents. While the sensors can be replaced and the energy consumption measured reliably, the new sensor couple will have a different measurement offset, which is not necessarily implemented in the utility meter.

This creates some significant challenges; to justify the cost of remotely read meters, utilities want to extract as much knowledge as possible from the vast amounts of data they provide. While valuable knowledge can be subtracted from the data as it is, more advanced analysis requires higher data quality to ensure the validity of the results; a data quality that the meter was never intended to provide.

Recognizing this challenge, the Danish Technological Institute, as part of the European research project FunSNM, has developed a groundbreaking method to address the situation. The solution lies in treating the entire collection of meters not as individual units, but as an interconnected network.

The core idea is simple yet powerful: physics doesn’t lie. The water temperature in a district heating network follows fundamental principles of energy conservation. It naturally decreases as it travels from the production plant, and this heat loss can be precisely modeled as a function of flow rate, ground temperature, and insulation levels of the pipes.

Figure 2: Sketch over the Unscented Kalman Filter. The “State Estimate” (meter offsets and service pipe insulation levels) is given. This, along with flows in the system, gives an “Expected Measurement” at each meter for the next time step. These are compared to the actual “Measurement”, and any differences (“Innovations”) are used to give an “Updated State”, which is used in the next cycle.

Our tool uses a sophisticated algorithm (an Unscented Kalman Filter, UKF) and a detailed physics model to build a dynamic digital twin of the network. The UKF works by calculating the expected temperature at all utility installations at each time. These temperatures are then compared to the actual measurements performed at the installations. When temperatures change during the day, the UKF can simultaneously identify two key parameters:

This process isn’t a one-time calibration; it’s a continuous, dynamic update that allows the meters to effectively “correct” each other in real-time and to determine slow degradation of the insulation levels of the pipes.

Figure 3: Error in expected meter offset (left) and error in estimated insulation level (right) before and after analysis for one heating season. Prior to analysis, temperature offset errors are up to 1.5 °C, and insulation levels are off by almost 0.1 W/m/K. After the analysis, the temperature offset is below 0.5, and the estimated insulation level is down to 0.01 W/m/K. The analysis is carried out on synthetic data to determine the true meter offset and insulation level.

This self-calibration method is powerful, but it has some limitations:

The benefits of this network-based approach move heat meters far beyond their traditional role. For utilities, the advantages are immediate and tangible:

Ultimately, this transformation of meters into an intelligent sensor network is about more than just data – it’s about future-proofing district heating. As the sector moves towards lower supply temperatures and greater integration with renewable energy sources, network efficiency and precision become paramount.

By unlocking the hidden intelligence in existing infrastructure, utilities can make smarter investments, build lasting consumer trust, and secure the role of district heating as a cornerstone of the sustainable energy systems of tomorrow. Altogether, strengthening the potential to reduce supply temperatures, leading to even greater savings for utilities.

Senior Specialist, Danish Technological Institute

District heating is vital for the green transition in Denmark. Utilizing domain knowledge from District Heating, in combination with general physics, contributes to the value creation from utility meter data. This field is still quite new, and it is interesting to be part of it from the beginning and observe its development.

Consultant, Danish Technological Institute

Domestic district heating meters may be viewed as a collective sensor network. This poses an interesting problem, where it may be possible to use data to derive useful information about the district heating network that goes beyond the original data.

We believe that district heating utilities may benefit from allocating their resources to maintenance where they have the greatest impact. Knowing which segments of the district heating networks have the highest heat losses, it is possible to focus your resources there, rather than replacing the oldest pipes first. Likewise for the utility meters. Consumers need to trust the devices used to bill them. Novel methods for evaluating measurement accuracy may help ensure reliability and fairness for customers.

The post From Billing Tools to Network Brains: UNLOCKING THE HIDDEN VALUE IN YOUR HEAT METERS first appeared on DBDH.

]]>The post DEMOCRATIC OWNERSHIP IS NEEDED TO SCALE UP DISTRICT HEATING first appeared on DBDH.

]]>By Magnus Skovrind Pedersen, CEO of Think Tank Brundtland, and Lasse Skou Lindstad, analyst at Think Tank Brundtland.

Published in Hot Cool, edition no. 2/2026 | ISSN 0904 9681 |

Europe is entering the largest heat infrastructure expansion in modern history.

District heating will play a central role in the transition to renewable energy, energy independence, and a more flexible energy system. Most European countries are expected to expand their networks significantly in the coming decades.

How should Europe organize and finance this scale-up?

Commercial district heating investors who demand adequate returns are unwilling to make the necessary investments. This creates a structural financing gap between the investments we need and those that yield a high enough return to satisfy private investors. As a result, we instead need to promote democratic ownership structures, in the form of municipal and consumer-owned utilities, to deliver the necessary investments. The ability of democratically owned utilities to deliver the necessary investments is supported by evidence from the electricity sector, where publicly owned utilities invest more in renewable energy than their private counterparts.

Infrastructure transitions rarely fail because of engineering constraints. They stall because institutions are misaligned with investment needs.

A research team led by Daniel Møller Sneum recently examined barriers to the rollout of district heating [1]. The conclusion was clear: The most difficult and decisive barriers are economic and political. Not technical.

This finding is consistent with Brundtland’s [2] broader analytical work on energy infrastructure. When transitions require patient capital and governance of natural monopoly networks, ownership becomes central. Markets alone rarely deliver optimal outcomes without institutions that reduce risk and ensure legitimacy.

When it comes to assessing risk in the district heating sector, it is essential to distinguish between new and existing systems.

Existing systems benefit from established customer bases and stable operations. Risks are lower and more predictable.

New systems face uncertainty regarding customer uptake, regulatory stability, construction costs, and local capabilities. These uncertainties translate into financial risk.

In capital markets, higher risk directly translates into a higher required return to compensate. Preliminary evidence from research led by Daniel Møller Sneum shows an average required rate of return for commercial district heating investors of around 11%. [3]

In comparison, Heat Roadmap Europe 5 (HRE5) [4] , which outlines a cost-effective strategy to decarbonize heating in Europe, uses a real discount rate of 3% a year to evaluate investments. A discount rate is used to translate future costs and benefits into today’s value. It reflects that money today is worth more than money in the future. The 3% is a real rate (excluding inflation). With inflation of around 2%, this corresponds to a nominal rate of roughly 5%.

But since commercial district heating investors need a 11% return per year, many of the investments that Heat Roadmap Europe points to as necessary at a 5% rate will not be feasible for a commercial investor. This creates a structural financing gap between what society needs and what generates a high return.

From Brundtland’s perspective, this gap is not accidental. It reflects a mismatch between private risk assessment and public system value. District heating provides system benefits beyond individual project cash flows, including flexibility, energy security, strategic autonomy, and emission reductions. Yet these benefits are not fully captured in market pricing. While economists often argue that you can integrate all of these into the market price with the right taxes and subsidies, implementing them can be politically and technically difficult and may not be sufficient in time.

The solution is a different type of ownership that can value the true benefits of district heating. In other words, this requires consumer- and publicly owned district heating that can account for broader societal benefits when making investment decisions.

Therefore, if we want to achieve strategic energy autonomy and a green heating sector in Europe, we need democratic ownership.

While commercial district heating investors will be unwilling to invest in projects with medium or low returns, democratically owned district heating companies are not limited by the same need to maximize their short-term returns.

![Figure 1. Source: Think Tank Brundtland based on data from KommuneKredit , Danish District Heating Association [Gæ9.1], Heat Roadmap Europe 5, and preliminary results from Møller Sneum et al.](proxy.php?url=https://dbdh.org/wp-content/uploads/2026/03/Figure-1-1-e1773662605677.jpg)

Figure 1. Source: Think Tank Brundtland based on data from KommuneKredit [5], Danish District Heating Association [6], Heat Roadmap Europe 5, and preliminary results from Møller Sneum et al. [7]

As an example, a democratically owned Danish district heating company can get a loan of around 3.6% per year for a 30-year loan through the public credit institution called KommuneKredit. KommuneKredit borrows through sovereign bonds issued by the Danish central bank. Here, the Danish state can issue a 30-year bond with an interest rate of around 3%.

On top of that, the municipality that facilitates the KommuneKredit loan guarantees the loan and on average demands a yearly guarantee commission of around 0.6%. The combination of democratic ownership and the help of a public credit institution means that the district heating company can borrow at 3,6%. If the goal of an investment by a democratic district heating company is just to “break even”, then the investments in Heat Roadmap Europe 5 discounted at a rate of 5% become feasible.

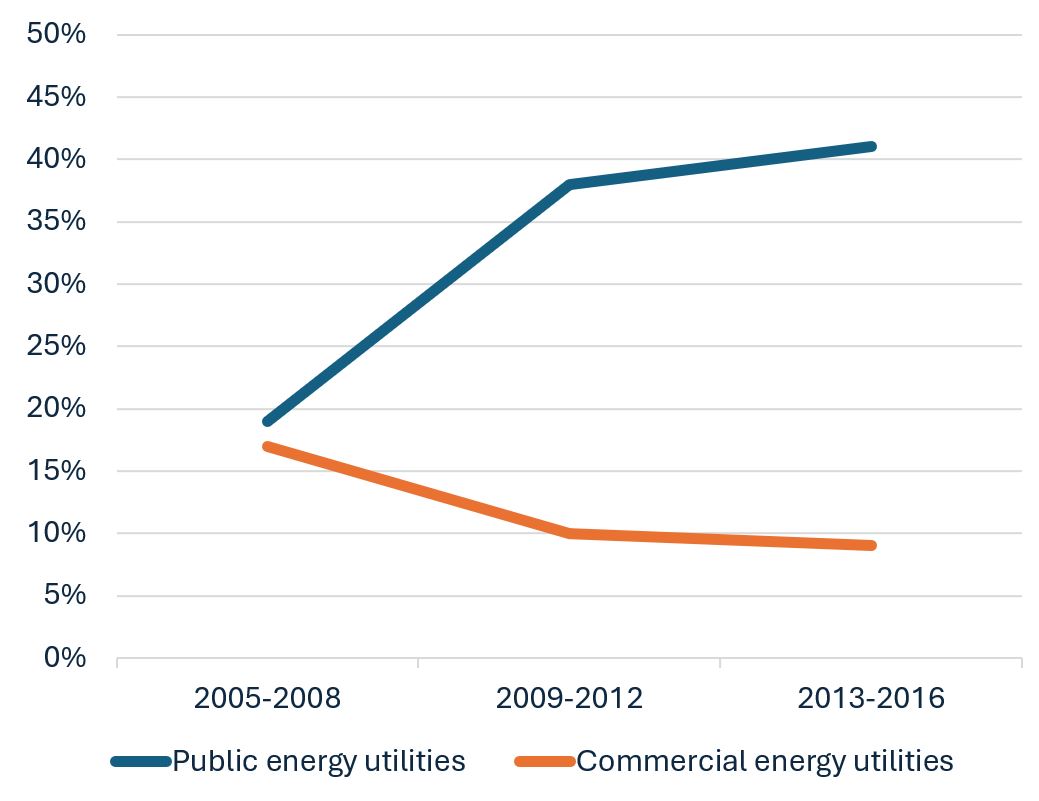

The ability of democratic ownership to increase green investments is confirmed by a growing literature. One study by Steffen et al. 2022 looked at energy utilities across Europe and found that public utilities had a significantly higher rate of investments going towards renewables. This study was based on power utilities, but some of their investments overlap with some district heating as well, such as biomass and geothermal energy.

Figure 2. Source: Think Tank Brundtland, based on Steffen et al. 2022 [8]

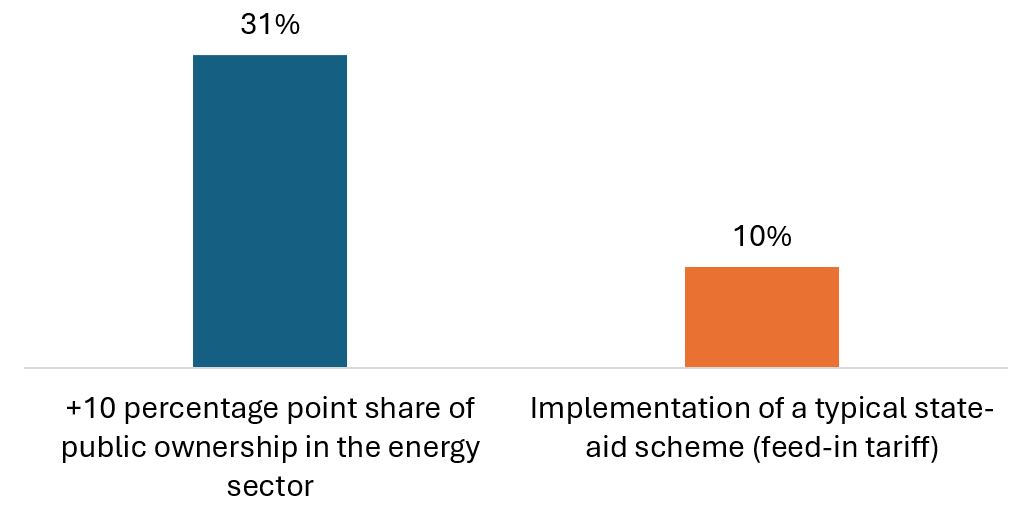

Likewise, research from the OECD has found that a higher level of public ownership among electric utilities is associated with significantly higher investment in renewables. A 10-percentage-point higher share of public ownership in the energy sector was associated with a 31% increase in investment in renewable energy. In comparison, introducing a typical state aid scheme for renewables, a feed-in tariff, was associated with a 10% increase in renewable investment.

Figure 3. Source: Think Tank Brundtland based on Prag et al. 2018 [9]

These results cannot necessarily be translated 1:1 to the district heating sector, but they point to the pivotal role of democratic ownership in accelerating and scaling the green transition.

Europe does not lack the necessary technology to expand district heating. It lacks the right institutional framework. Commercial investors who demand double-digit returns leave a structural gap between societal need and private profitability. Democratic ownership, on the other hand, has lower capital costs and required rates of return, enabling patient investment in the rollout of district heating. This is also supported by evidence from the power sector, where publicly owned utilities and companies invest more in renewables. If Europe wants rapid decarbonization, energy security, and strategic autonomy, democratic ownership is essential.

The post DEMOCRATIC OWNERSHIP IS NEEDED TO SCALE UP DISTRICT HEATING first appeared on DBDH.

]]>The post MPEC OSTRODA, POLAND – GOING GREEN first appeared on DBDH.

]]>By Wojciech Zalewski, CEO MPEC Ostróda, Lars Gullev, CEO Gullev DH Advisory, and Mathias Vestergaard Steenstrup, Project Manager – DH Specialist, Artelia

Published in Hot Cool, edition no. 2/2026 | ISSN 0904 9681 |

In autumn 2023, in connection with work for the Danish Embassy in Warsaw, with a focus on supporting the green transition of district heating (DH) companies in Gliwice and Gdynia, the district heating company MPEC Ostróda was visited. A DH company with committed management that clearly saw the need for a green transition of heat production. Not only to be green, but primarily to ensure that customers’ DH price remained competitive with alternative heating methods. Rising coal costs, including CO2 quota costs, would threat-en a future competitive DH price.

An application to the Danish Energy Agency (DEA) for support in preparing a Development Plan for MPEC Ostroda and continued close cooperation with PEC Gliwice and the Gliwice municipality was submitted in autumn 2023, approved by DEA just before Christmas 2023, and preparation of the Development Plan started in early 2024.

The project aimed to plan the green transition for a sustainable and efficient DH system. MPEC Ostróda also aimed to maintain a low, stable heat price for its consumers and a high level of security of supply, while, as a frontrunner, making the transition from a fossil-fuel-based to a sustainable, efficient DH production.

Signing of the MoU between MPEC Ostróda and DBDH during His Majesty the King of Denmark’s visit to Poland in January 2024. From left to right: Ole Toft, former Danish ambassador in Poland, Wojciech Zalewski, CEO MPEC Ostróda, Lars Aagaard, Danish Minister of Energy & Climate, Pia Zimmermann, Export Manager, DBDH, and His Majesty King Frederik X.

Changes in broader environmental policies and the Russian invasion of Ukraine in February 2022 have had a significant impact, completely changing the approach to heating in Ostróda.

The years 2022–2024 marked a turning point. Prices of coal, electricity, and natural gas surged dramatically, with costs climbing almost daily. Heating prices for residents reached unprecedented levels, setting a new record for the company. The company’s aim became to survive in the market.

Following these events, the company decided to invest quickly in new heating production to reduce heating costs for residents in Ostróda. Thus, the company and the city of Ostróda in 2024 invested in a 4.6 MW biomass boiler – the first sustainable heat production source in the history of the company, not subject to CO2 taxes.

The company changed its natural gas and electricity contracting policies for its combined heat and power (CHP) operations, partnering with the Finnish company FORTUM, thus start-ing a new chapter in its operations. The new cooperation principles and stock market con-tracting brought the first results by the end of 2023, as the company presented a significant profit from sales of electricity, which helped cover the loss from coal-based production – main-ly CO2-related expenses.

But it didn’t stop there. Since October 2023, MPEC Ostróda has been establishing a 10 MW natural gas-fired boiler. The tender closed in March 2024, the contract was signed in April 2024, and the boiler went into operation at the beginning of 2025 (figure 1).

Figure 1: Sankey diagram of the energy mix – Simulation 2025.

In addition to significant investments, the development has required support from consumers and, not least, from political institutions. These potential barriers have been identified, allowing them to be addressed to achieve a sustainable and efficient DH supply in Ostróda.

MPEC Ostróda has started addressing these barriers by releasing a short video about the DH company and explaining that its investments, together with changes in fuel prices, have led to an 18% decrease in the heat price since 2024.

The shares of coal, natural gas to CHP, natural gas to boiler, and biomass in 2025 were 15%, 24%, 26%, and 35%, respectively (Figure 2).

Figure 2: 2025 heat production – natural gas for CHP, biomass, natural gas for boiler, and coal.

In accordance with the EED, the current energy mix will be insufficient and not fulfill the requirements by January 2027 (see text box below).

The objectives of MPEC Ostróda – as mentioned in the text box – are highly related to the revised Energy Efficiency Directive (EED) of the EU. The EED is a directive of the EU that aims to improve energy efficiency in all member states. Introduced in 2012, the directive has undergone several revisions, with the most recent update in 2023, which integrated it into the Fit for 55 package and the European Green Deal – key strategic and legislative frameworks for reducing CO₂ emissions.

Under the EED, efficient heat supply systems must meet the criteria mentioned in the text box.

To set up a development plan [MD8.1][la8.2]for MPEC Ostróda, it was necessary to perform a detailed techno-economic analysis. Implementation of new green production capacity and new technologies requires a thorough understanding of the varied production and heat de-mand, as well as the costs of production. Changes in heat demand and production capacity were analysed using an annual simulation model.

The model was built and simulated in EnergyPRO – a leading software for detailed modeling and simulation of energy systems. The software offers tools for users to conduct feasibility studies, financial analysis, energy production and distribution optimisation, and evaluate op-erational scenarios.

In the software, a wide range of technologies for integrating and analysing various systems can be selected, including large-scale heat pumps, electric boilers, heat storage, geothermal energy, and renewable energy sources such as wind and solar power.

By comparing the model and simulation results with the actual energy mix and operating costs, a reference operating cost was determined.

By running several simulations with iterating capacities and combinations, the most economi-cally and practically feasible solution for a sustainable and efficient DH supply of MPEC Os-tróda was identified for 2030. The following mix also considers fuel diversity and efficiency, as was pointed out in the strategy (figure 3).

Figure 3: Sankey diagram of the energy mix of the 2030 model and simulation.

By addressing all criteria and conditions, a roadmap (fig. 4) for MPEC Ostróda to meet the EED criteria and to have a more sustainable and efficient supply of DH, was made.

Figure 4 Roadmap 2030 of investments needed to obtain a sustainable and efficient DH supply.

Through the development of a strategy aiming to implement a sustainable and efficient DH supply, criteria for procedures and investments have been found. These criteria will ensure a future DH system that is economically feasible and technically sufficient.

The techno-economic evaluation has shown that a mix of solar thermal collectors, heat pumps, and the existing biomass boiler and CHP unit, together with thermal energy storage capacity, is an optimal solution.

Figure 5: Simulated shares of production of MPEC Ostróda in 2030.

Based on the requirements of the EED and projected share of RES in the electricity sector, MPEC Ostróda’s simulated share of RES from heat production is 66%, fulfilling both the re-quirements of 2028 and 2035.

Also, the share of RES and high-efficiency CHP combined amounts to 85%, fulfilling the re-quirements of 2035. However, this requires a slight increase in the efficiency of the two CHP units at MPEC Ostróda. An overview of the contributions from each production unit is shown in Fig. 5.

Based on the production share shown above (Fig. 4), the total CO2 emissions amount to 8,400 t/year. The reduction in CO2 emissions corresponds to 59%.

Therefore, the aim of CO2 emissions (see text box) by MPEX Ostróda is not met. However, most CO2 emissions come from CHP, which is considered efficient and contributes to a greener electricity supply in Poland.

All in all, the green transformation of MPEC Ostróda is a fine example of how visionary management can translate vision into action, while the investments made lay the foundation for a still-competitive district heating price. Without the green transformation, MPEC Ostróda would not have been able to deliver a competitive product to its customers.

The experience from MPEC Ostroda can be used in many district heating companies in Poland and other countries. So, use your personal network to exchange experiences. This way, the green transition can be made more affordable for customers, society, and the environment.

The post MPEC OSTRODA, POLAND – GOING GREEN first appeared on DBDH.

]]>The post HORSENS DISTRICT HEATING SCALES UP GREEN HEAT SUPPLY WHILE TRIPLING ITS CUSTOMER BASE first appeared on DBDH.

]]> Curious to learn more?Read the latest industry news on dbdh.org here.

The post HORSENS DISTRICT HEATING SCALES UP GREEN HEAT SUPPLY WHILE TRIPLING ITS CUSTOMER BASE first appeared on DBDH.

]]>