The post JPMorgan Healthcare Conference Week Recap and 2026 Outlook appeared first on The Dedham Group.

]]>

By Sachin Purwar, Mike Hamlin, & Sophia Tan

The 44th Annual J.P. Morgan Healthcare Conference (JPM 2026) and its sister conference, Biotech Showcase, concluded in San Francisco on January 15, signaling a year defined by disciplined growth, sharpened strategic execution, maturing innovation, and heightened geopolitical complexity. Across pharma, biotech, MedTech, digital health, and healthcare services, leaders expressed measured optimism rooted in strong scientific momentum and improved capital conditions—tempered by policy uncertainty and global competitive shifts.

1. Dealmaking Trends: Selective, Strategic, and Value‑Focused

While headline‑grabbing mega‑mergers were limited during JPM week, dealmaking sentiment strengthened meaningfully. Strong Q4 2025 momentum, readily deployable capital, and improving public-market conditions are driving a shift toward high-quality, strategically aligned transactions.

Key Trends:

- Licensing over mega M&A:

Large biopharma is prioritizing targeted, high‑impact licensing deals and bolt‑on acquisitions that reinforce pipeline strategy, rather than pursuing transformative mergers.

- IPO window is reopening:

Late‑2025 momentum (157% jump in Q4 IPO volume) and early‑2026 offerings (Aktis’ $318m offering in early January immediately followed by Eikon and Veradermics announcing their IPO plans) are signaling renewed investor appetite.

- Disciplined capital deployment:

Companies are leaning toward later‑stage, de‑risked assets, differentiated innovation (particularly from China), and programs aligned with upcoming patent cliffs, emphasizing quality over quantity.

Takeaway:

Capital is available—but discipline governs decisions. Transactions will increasingly favor assets offering clear strategic fit, differentiation, and line‑of‑sight to value.

2026 Outlook:

- Premiums will concentrate around high‑quality, late‑stage programs.

- Early‑stage companies must show stronger validation to attract interest.

- Competition for differentiated assets will intensify as patent cliffs approach.

2. China’s Biotech Rise: Reshaping Global Competition

China’s presence at JPM was impossible to ignore. For the first time, discussions positioned China not as a fast follower but as a frontline innovator across modalities, clinical execution, and pipeline diversification. Western companies increasingly rely on Chinese assets to fill pipelines, while China accelerates in complex modalities and clinical execution.

Key Trends:

- Acceleration in licensing activity:

Nearly half of U.S./EU in‑licensing deals in 2025 involved Chinese‑developed pipelines, including major deals such as Pfizer – 3SBio, GSK – Hengrui, and Novartis – Argo. The first few weeks of 2026 already produced major deals including Abbvie – RemeGen (up to $5.6b) and AstraZeneca – CSPC (up to $18.5b).

- Leadership in complex modalities:

Chinese biotechs are increasingly at the forefront in ADCs, bispecifics, RNAi, cell therapy, and gene therapy—driven by robust scientific talent, aggressive investment, and maturing clinical capabilities.

- Development & cost efficiencies:

Faster patient enrollment, lower trial costs, and accelerated data generation are drawing Western companies toward China as both a partner and a competitor.

Takeaway:

China is now a central force in global biopharma—an indispensable innovation hub, a formidable competitor, and a critical strategic variable.

2026 Outlook:

- Expect expanded East‑West collaborations in high‑value therapeutic areas.

- Global scouting strategies must treat China as a primary—rather than secondary—source of innovation.

- Competitive pressure will rise as China continues moving decisively into frontline innovation.

3. Policy & Geopolitics: The New Strategic Wild Cards

Policy and geopolitical dynamics shaped a significant share of discussions at JPM 2026. Pricing reforms, IRA implementation, and U.S.–China tensions are now strategic determinants—not background noise.

Key Trends:

- Pricing reform reshaping valuation:

Most Favored Nation (MFN) pricing proposals and Inflation Reduction Act (IRA) implementation are influencing launch sequencing, global price corridors, and long‑term asset valuation

- Geopolitical implications:

The geopolitical uncertainties and tension are affecting supply chain design, data governance strategies, and cross‑border investment.

- Policy risk mitigation:

Companies are building policy risk directly into portfolio and geographic planning to mitigate volatility.

Takeaway:

Policy and geopolitics now sit at the center of strategic planning instead of the periphery.

2026 Outlook:

- Portfolios must be stress‑tested against varying pricing and reimbursement scenarios.

- Cross‑border dealmaking will become more cautious and selective, requiring stronger policy fluency.

- Supply chain resilience and geographic diversification will be imperative.

4. AI: Shifting From “Hype Cycle” to “Proof Cycle”

AI has shifted from theoretical promise to measurable enterprise value. Companies showcased real‑world impact across discovery, clinical development, strategic decision making, and operations. At JPM 2026, companies emphasized AI’s ability to accelerate timelines, optimize resources, and de-risk development.

Key Trends:

- Discovery accelerator:

AI is compressing discovery timelines and improving target and molecule design, which are especially impactful in complex therapeutic areas.

- Clinical development efficiency:

Clinical trials are becoming more efficient through AI‑driven patient recruitment, site selection, adaptive trial design, protocol optimization, and responder identification and stratification.

- Enterprise strategy optimization:

Organizations are embedding AI into portfolio prioritization, BD targeting, commercial forecasting, and manufacturing/supply chain optimization.

Takeaway:

AI is now a core driver of scientific and operational advantage. Execution maturity—not ambition—will differentiate leaders from laggards.

2026 Outlook:

- AI‑enabled platforms will become standard across R&D and operations.

- Companies with deeper AI integration will command premium valuations.

- BD teams will increasingly evaluate AI capabilities as part of partner diligence.

5. Emerging Modalities: The Next Wave of Differentiation

JPM 2026 highlighted multiple high‑growth therapeutic and modality areas poised to reshape the industry. These fields combine scientific complexity with strong commercial potential.

Key Trends:

- ADCs & bispecifics:

Continue to dominate oncology innovation as strong late‑stage data reinforces their role in next‑generation oncology portfolios

- Aging, longevity, & brain health:

Gaining traction as biomarkers mature and aging is reframed as a modifiable biological process.

- Women’s health:

Renewed focus on an underfunded, high‑value space—including reproductive health, menopause, and sex‑specific disorders.

- Radiopharmaceuticals, RNA therapeutics, and gene editing:

Accelerating through clinical pipelines with strategic partnerships accelerating development and commercialization.

Takeaway:

Emerging modalities represent the next frontier of precision medicine and early movers will gain durable scientific and commercial advantage.

2026 Outlook:

- Heightened competition for differentiated oncology, neurology, and women’s health platforms.

- Partnerships will remain essential to access novel modalities and mitigate development risk.

- Modality selection will become a core strategic lever for long‑term differentiation and investors will reward platforms with validated biology and clear clinical paths.

Conclusion:

JPM 2026 delivered a clear message: innovation is booming, but disciplined execution will determine who wins.

Success in 2026 will depend on the ability to:

- Strengthen pipelines through targeted, data‑driven dealmaking

- Compete and collaborate effectively in a China‑accelerated global landscape

- Successfully incorporate and demonstrate ROI in AI and digital transformation

- Scale precision medicine and next‑generation modalities

- Navigate policy and pricing headwinds without slowing innovation

- Build validated business cases for assets that withstand market, regulatory, and investor/partner scrutiny

As the industry enters a year marked by opportunity and complexity, the organizations that thrive will be those that pair strategic clarity with rigorous execution.

The Dedham Group partners with biopharma leaders to develop data-driven insights, anticipate market shifts, optimize commercial strategy, and unlock value across emerging therapeutic and modality landscapes. We welcome the opportunity to discuss how your organization can position itself for success in 2026 and beyond.

About the Authors

- Mike Hamlin, Associate Partner | Email: [email protected]

- Sachin Purwar, Partner | Email: [email protected]

- Sophia Tan, Managing Partner | Email: [email protected]

The post JPMorgan Healthcare Conference Week Recap and 2026 Outlook appeared first on The Dedham Group.

]]>The post White Paper: The Rise of Direct-to-Patient appeared first on The Dedham Group.

]]>The post White Paper: The Rise of Direct-to-Patient appeared first on The Dedham Group.

]]>The post AI and The Next Wave of Alert Fatigue in Oncology? appeared first on The Dedham Group.

]]>

As oncology becomes more data-driven, the burden of navigating complex digital workflows is growing. While “click fatigue” has long been cited as a byproduct of evidence-based pathways and clinical decision support tools, we’re now entering a new phase, one where pop-up fatigue may emerge as a more disruptive force.

Unlike passive documentation burdens, this wave is shaped by active, real-time alerts injected into the physician workflow, increasingly from AI platforms analyzing data in the background.

From Pathways to Pop-Ups

Companies like Tempus, Viz.ai, and OncoLens are embedding their AI engines into the EHR, surfacing alerts to identify clinical trial eligibility, treatment opportunities, or adverse events. These tools are powerful and have already demonstrated a positive impact for many cancer patients, often parsing unstructured data and labs to identify patterns a human might miss. As we say often in healthcare, however, these dynamics don’t operate in isolation.

Consider the recent partnership between Tempus and Stemline Therapeutics: Tempus’s AI scans patient records to flag potential candidates for Orserdu and generating real-time alerts that appear within a physician’s workflow¹. In a silo, that is incredibly valuable information. However, if these pop-ups layered onto simultaneous alerts from the EHR vendor, drug safety flags from integrated compendia, and institution-specific pathway nudges, it is easy to see how this can result in an overwhelming number of pop-ups.

In one JAMA Oncology study, researchers tested different EHR alert designs for prompting serious illness conversations in gynecologic oncology. They found that required alerts did improve response rates, but also increased workflow interruption and clinician frustration². In other words, even good alerts still contributed to fatigue when delivered at the wrong moment or without sufficient context.

Alert Fatigue, Amplified

The underlying risk isn’t just inconvenience, it’s cognitive overload. When clinicians see too many alerts, even important ones may get dismissed. A study on EHR-based trigger systems for cancer diagnosis delays highlighted this: although the triggers improved detection, the research team noted that without precise tuning and prioritization, alerts quickly became “background noise”³.

With multiple platforms potentially injecting signals into the same workflow, the probability of alert redundancy rises dramatically. If two different AI systems flag the same patient for two similar reasons, without coordination, providers may start tuning them all out.

The scale of the problem is already visible. A recent analysis of oncology specialists’ inbox use found a 19% increase in message volume and a 16% increase in EHR time from 2019 to 2022⁴ highlighting that clinician digital burden continues to climb.

Where Do We Go From Here?

The challenge isn’t just to limit alerts, but to make them smarter.

- Relevance Over Volume: Every alert should have a clearly defined purpose and a high likelihood of driving action.

- Context-Aware Timing: Alerts should be delivered at the right moment—not during documentation or order entry, but when clinicians are making related decisions.

- Precision Targeting: Instead of sending the same alert to every oncologist, systems should be able to route insights to the most relevant specialist based on role, disease state, or prior interaction with the patient.

Ultimately, the future of AI in oncology depends not just on what it can find, but on how, when, and why it chooses to speak up.

References

- Tempus and Stemline Therapeutics collaboration announcement. Tempus press release, Feb 2025.

- Patel MI, Sundaram V, Desai M, et al. Long-term Effect of Machine Learning-Triggered Behavioral Nudges on Serious Illness Conversations in Oncology. JAMA Oncology. 2022. Link

- Singh H, El-Kareh R, Thomas EJ, et al. Electronic health record-based triggers to detect potential delays in cancer diagnosis. BMJ Qual Saf. 2013. Link

- Tai-Seale M, Dillon EC, Yang Y, et al. National Trends in Oncology Specialists’ Electronic Health Record Inbox Work, 2019–2022. JAMA Network Open. 2025. Link

The post AI and The Next Wave of Alert Fatigue in Oncology? appeared first on The Dedham Group.

]]>The post Bridging the Gap: Navigating Oncology Provider Hub and Satellite Site Dynamics appeared first on The Dedham Group.

]]>

By Casey Speer, Principal & Miranda Brekke, Senior Consultant

In today’s increasingly complex oncology landscape, manufacturers face mounting pressure to launch innovative therapies and optimize adoption for eligible patients across all care settings. An overlooked, yet critical, lever for improving novel product adoption is a deeper understanding of provider hub and satellite site dynamics.

Satellite Opportunity

Many provider organizations today operate under a hub and satellite structure, where a central academic or high-volume community “hub” site is surrounded by smaller “satellite” treatment centers. While hubs often serve as centers of excellence with high patient volumes and complex care capabilities, satellites present unique challenges for patient care as they frequently cater to more localized populations and often manage routine or less complex aspects of care.

Variability in Hub and Satellite Models

It’s important to note variability in hub and satellite models across sites of care. While institutions generally have a centralized hub, community practices function more loosely with one or more “main” site(s) based on patient volume and location. Regardless of model, satellite sites present as a key opportunity for meaningful uptake given increased convenience, geographical reach and untapped patient volume.

When evaluating hub and satellite model variability, the following factors should be considered:

- Provider Specialization: The extent of provider specialization dispersed across sites may vary, as some models have specialists broadly across satellites while others centralize specialists to the hub.

- Decision-Making Power: In some organizations, therapeutic decisions are centralized and made at the hub level; in others, satellites operate more independently.

- Treatment Location: Actual location of treatment may start at the hub and transition to a satellite for ongoing care, or remain local throughout.

For manufacturers, identifying these models and potential impact on portfolio brand adoption is essential for designing appropriate education & support strategies.

The Problem: Limited Novel Product Adoption Across Satellites

Within oncology, novel product adoption at satellite sites remains inconsistent despite increased patient convenience and patient potential. This is due to several systemic challenges:

- Limited Experience: Satellite providers often have less familiarity with novel therapies, impacting data awareness and comfortability with safety and tolerability profiles and leading to decreased adoption of newly approved, innovative therapies.

- Operational Barriers: Distance from hubs, referral relationships, and poor hub coordination / communication create disconnects.

- Awareness and Familiarity Gaps: Satellites may not have the same access to training or updated protocols.

Limited adoption of novel treatment regimens across satellites is most consistently seen across complex oncology regimens which may require additional infrastructure or accreditations to administer therapy (e.g., monitoring, REMS requirement, advanced AE management, etc.), leading to greater satellite reliance on hub sites. Manufacturers must not only ensure these therapies are accessible at hub sites but also equip satellites to handle them confidently.

Solutions: Top-Down and Bottom-Up Support

To bridge the gap between hub and satellite novel product adoption, manufacturers can aim to support organization-wide standardization efforts with direct-to-account and top-down support. For example, direct-to-account support may include clinical pathways refinement & protocol development, while top-down support may target networks, aggregators & societies. Additionally, driving satellite-level interest (e.g., champion activation, best practice sharing, value messaging, etc.) has proven to be critical for complex therapy adoption in oncology.

Strategic Takeaway: Targeted Education & Support by Model

As more patients are seen closer to home & outside of hub locations, manufacturers must move beyond traditional support strategies and target efforts on novel product adoption across high impact satellite sites. Success hinges on understanding how each hub and satellite model operates, considering how and where decisions are made, and tailoring education & support strategies accordingly.

The post Bridging the Gap: Navigating Oncology Provider Hub and Satellite Site Dynamics appeared first on The Dedham Group.

]]>The post What Makes a ‘Next-Generation’ Oncology Therapy? Data, Differentiation and the Power of Positioning appeared first on The Dedham Group.

]]>

By Matthew Cunningham, Managing Partner

In oncology, the language used to frame innovation matters. Terms like “next-generation,” “second-generation,” and even “third-” or “fourth-generation” are used to imply progress—but they also influence how products are perceived by providers, payers, and investors.

The use of these terms is not just siloed to post-launch marketing —it’s growing significantly in the scientific literature.

Framing Innovation: A Growing Trend in Scientific Literature

A PubMed analysis* of over 18,000 therapeutic-focused publications from 2010 to 2024 shows that title references to “next-generation,” “second-generation,” “third-generation,” and “fourth-generation” have all increased significantly.

While the analysis spans multiple therapeutic areas, this trend is highly relevant for oncology, where generational labels can carry implications for market positioning, payer coverage, and trial design. While “next-generation” remains the most commonly used term, recent years show a sharp uptick in “third-” and “fourth-generation” verbiage—signaling deeper class maturity.

What Does “Next-Generation” Actually Mean?

While ordinal generations (e.g., second, third, fourth) typically represent the ability to overcome a resistance mechanism or have clean clinical superiority, the term “next-generation” lacks consensus or regularity definition. In practice, it’s often used to indicate one or more of the following:

- Mechanistic refinement (e.g. increased selectivity, novel binding)

- Activity in resistant disease

- Improved safety/tolerability

- Operational benefits (e.g. subcutaneous vs. IV, fewer doses)

The question arises, how much better is “next”? The answer many times depends on who you are asking and in what context.

Clear-Cut Examples

For many “next gen” oncology therapies, the label is non-controversial and represents a legitimate leap forward in standard of care. Examples such as Tagrisso (third-generation EGFR-TKI) Brukinsa / Calquence (second-generation BTK inhibitors) and Enhertu (next-generation ADC) clearly moved standard of care forward and had mechanistic rationale for improvement over prior generations.

Future-State Murkiness and Strategic Tradeoffs

Calling a therapy “next-generation” does more than signal innovation—it anchors the product within the same mechanistic class as its predecessor. In novel modalities like bispecifics, cell therapies, or modular immunotherapies, it becomes much harder to define what “next-generation” actually means. Mechanisms of action are more complex, targets are often novel or combinatorial, and the biology may not map cleanly onto earlier standards of care. In these cases, generational language can blur the line between true class evolution and mechanistic reinvention.

Once a product is positioned as the next generation of an existing therapy, it’s naturally evaluated in direct comparison to what came before—not just by providers, but by payers as well. Even when clinical differentiation is well-established, payers may still look to manage the class as a whole, either through direct management, or pricing and contracting pressure.

This tension will become even more pronounced in the red-hot field of PD-(L)1 bispecifics. Describing these bispecifics as “next-generation checkpoint inhibitors” may sound progressive, but it implies some degree of class continuity vs. an entirely novel therapeutic. As immunotherapies such as Keytruda & Opdivo approach biosimilar entry & IRA pressure, maximizing the differentiation of bispecifics can help insulate from inevitable pricing & payer management pressures in the PD-L1 class.

As more complex oncology therapies enter the market, navigating the balance between innovation and class inheritance will only grow in importance within manufacturer positioning & differentiation strategies.

*Methodology Note

PubMed records were extracted using the following title search terms: “next-generation”, “second-generation”, “third-generation”, and “fourth-generation” (with and without hyphens). Titles were filtered to exclude non-therapeutic domains such as education, nursing, policy, engineering, workforce development, testing and sequencing.

Entries were retained only if the title included therapeutic or biomedical keywords such as: therapy, therapeutic, treatment, cancer, tumor, leukemia, CAR-T, checkpoint, biologic, inhibitor, target, antibody, drug, oncology, lymphoma, immune, mutation, adjuvant, chemotherapy, or metastatic.

The post What Makes a ‘Next-Generation’ Oncology Therapy? Data, Differentiation and the Power of Positioning appeared first on The Dedham Group.

]]>The post From Policy to Practice: Strategically Navigating Maximum Fair Price Implementation appeared first on The Dedham Group.

]]>

By Rebecca Leemputte and Brady Stiller

The Inflation Reduction Act’s (IRA) Maximum Fair Price (MFP) provision enables the Centers for Medicare & Medicaid Services to negotiate prices for highly utilized drugs, representing a transformative shift in Medicare’s approach to drug pricing. Starting in 2026, MFPs will take effect for 10 high-volume Part D drugs and will expand in subsequent years to include additional Part D and Part B drugs. The magnitude of negotiated discounts is significant, with an average discount of over 50% for first-round drugs that treat diabetes, cardiovascular diseases, autoimmune diseases, and blood cancers.

While intended to make medications more affordable for beneficiaries, the implementation of MFPs will give rise to many unintended consequences that will disrupt patient access to medications. Top among these concerns are pharmacies not stocking and dispensing selected drugs and even community pharmacy closures resulting from material cash flow constraints, reduced profitability due to lower MFP-based reimbursement, and additional administrative workload.

Manufacturers will need to make strategic decisions on MFP effectuation to ensure continued therapy access in an environment with evolving drug purchasing workflows, channel economics, and brand access dynamics.

Prospective vs. Retrospective MFP Effectuation: Implementation Options & Risks

CMS guidance provides manufacturers with the option of effectuating MFPs prospectively or retrospectively. This decision will have significant impacts on pharmacy operations, brand access, patient experience, and manufacturer visibility.

With prospective MFP effectuation, pharmacies will purchase selected drugs at MFP. While pharmacies will benefit from reduced cash outlays given upfront purchasing at a significant discount, MFP inventory must be managed separately to avoid dispensing to ineligible patients. For manufacturers, this model is expected to pose challenges in tracking MFP dispensing and verifying patient eligibility, similar to challenges experienced with the 340B program today. Given anticipated program oversight and compliance monitoring limitations with the prospective model, it is likely that many manufacturers will opt for a retrospective effectuation model.

With retrospective MFP effectuation, pharmacies will purchase products at list price, payers will provide MFP-based reimbursement, and manufacturers will retroactively transmit a rebate to pharmacies following MFP eligibility validation, resulting in a net acquisition cost of MFP. While this effectuation model enables greater manufacturer control over patient eligibility validation, it will introduce significant financial and operational challenges for pharmacies:

- Pharmacy Cash Flow Issues: Many pharmacies will experience cash flow constraints while waiting for the MFP rebate beyond typical Medicare reimbursement timelines

- Pharmacy Administrative Workload: Pharmacies must establish new operational workflows to track and dispute rebate payments, which requires additional staffing and resources

- Pharmacy Profitability Impact: Many pharmacies currently experiencing favorable Medicare reimbursement margins may experience reduced profitability due to lower MFP-based reimbursement, with the magnitude of impact being influenced by manufacturer approach to rebate calculations

For manufacturers, the retrospective model also comes with risks:

- Brand Access Risks: As a result of the above financial and operational challenges, pharmacies may struggle to dispense selected drugs and maintain their business models, with downstream effects for patient access to medications

- Risk of Duplicative MFP & 340B Discounts: Since manufacturers must only provide the lower of MFP and the 340B ceiling price, manufacturers must validate claims for which a MFP rebate is required to avoid offering duplicate discounts, requiring sufficient levels of 340B claims visibility

- Compliance Risks For MFP Rebate Calculation & Transmission: Manufacturers must calculate the proper rebate amount and transmit the rebate within the designated prompt pay window to remain compliant

MFP effectuation model decisions will significantly impact pharmacy operations, brand access, and manufacturer compliance across multiple government pricing programs. It is essential that manufacturers address these risks with a proactive, strategic approach to ensure continued therapy access and maintain compliance.

Next Steps for MFP: Key CMS Deadlines and Risks Manufacturers Must Address

By September 1 of this year, first-round manufacturers must develop an extensive effectuation plan to comply with CMS requirements.

When developing an effectuation plan, manufacturers should proactively address the following questions regarding customer and brand access risks as well as compliance:

- What key operational and financial challenges will our distributor and pharmacy partners face due to our MFP effectuation strategy?

- What is our plan for helping customers navigate and minimize these challenges to support continued brand access?

- How will we maintain oversight across multiple pricing programs (e.g., 340B, MFP) to maintain compliance and ensure programs are used for appropriate patients?

Without a robust MFP effectuation plan, patients face significant risks of disrupted access to critical medications. It is imperative that manufacturers collaborate with pharmacies and distributors to implement strategies that ensure uninterrupted access and navigate the increasingly complex and evolving access landscape.

Need advice for navigating your MFP effectuation strategies? The Dedham Group can help. Contact us.

About the Authors

Rebecca Leemputte is an Associate Partner at The Dedham Group. Email her at [email protected].

Brady Stiller is a Senior Consultant at The Dedham Group. Email him at [email protected].

The post From Policy to Practice: Strategically Navigating Maximum Fair Price Implementation appeared first on The Dedham Group.

]]>The post What Gastroenterology Practice Consolidation Means for Pharma Manufacturers appeared first on The Dedham Group.

]]>

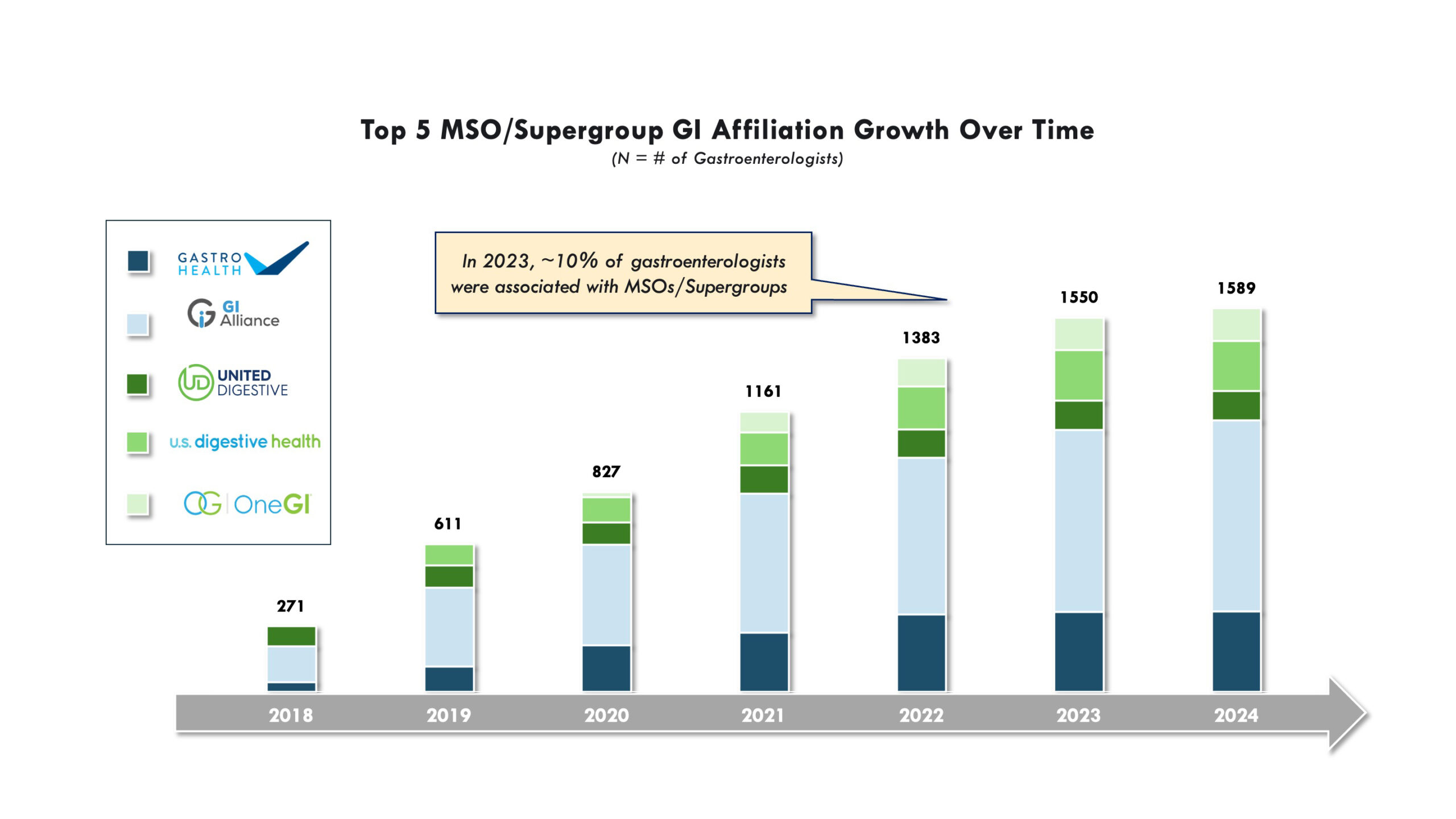

By Kelsey Smart and Daniel Colacurcio, PhD

A significant feature of the gastroenterology practice landscape is the ongoing consolidation process, seen at both national and regional levels. Central groups driving this trend are management service organizations (MSOs), which play a crucial role in practice consolidation along with an array of internal changes among growing rosters of member practices. These MSOs (also referred to as practice networks, aggregators, or super-groups) continue to expand their reach and influence through consolidation of member practices, but also lead “top down” changes among members. MSOs are increasingly investing in practice infrastructure, driving standardization of care, leveraging clinical specialists, and promoting data collection and clinical trial initiatives. Simultaneously, these larger consolidated groups are also exerting influence on relationships with regional payers and pharma.

As these MSOs continue to shape the gastroenterology practice sector, pharma is adapting to address this evolving customer segment. Here’s what these shifting dynamics mean for pharma manufacturers.

Consolidation & Expansion: Private Equity & MSOs in Gastroenterology

Private equity firms have made significant investments in the gastroenterology practice space, with MSOs as the primary groups driving change. Since 2016, several MSOs have emerged, with most backed by large private equity firms. Major players like GI Alliance, the largest physician-owned GI services group in the U.S. that represents over 800 gastroenterology specialists, and GastroHealth (which has acquired over 120 practices and 350 gastroenterology specialists) are large and unified groups compared to their smaller and more fragmented predecessors.

After acquiring small to mid-sized practices, PE firms and MSOs aim to streamline internal operations, create efficiencies, reduce costs, and enhance negotiating power with payers. For example, a large MSO may have a dedicated office of prior authorization specialists which can support prescribers across an entire network of practices, reducing the time which the gastroenterologists previously had to devote to administrative tasks. When successfully applied, such approaches allow gastroenterologists to focus more on patient care, particularly when “per hour” practice financial efficiency is closely linked to HCP availability to perform medical procedures and dedicate time to their patients.

Centralization & Efficiency: MSO Impact on Member Practices

MSOs provide critical administrative support across member practices, from billing and IT/EHR, to human resources and hiring. MSOs usually follow a centralized structure, which allows their network of practices to focus on specific treatment areas—such as inflammatory bowel disease through hiring and leverage of specialists. The dedicated focus on “center of excellence” development within practice networks has significant potential to consolidate leading clinical specialists in the community setting, parallel to those seen in academic-aligned hospital systems.

MSOs can accelerate the integration of novel treatments into clinical guidelines though organizational support for newer types of treatments, including biologics and recently-FDA approved options. Simultaneously, cutting-edge patient support and monitoring approaches can be formally put into practice to aid in the administration of these newer therapies. An MSO can also leverage their key opinion leaders to create internal referral networks to support HCPs across the organization for specialized consults, allowing “top down” influence of recognized clinical thought leaders and reduced variability in care across individual HCPs and practices.

Shifting Dynamics: What Does This Mean for Pharmaceutical Manufacturers?

As gastroenterology practice consolidation continues, pharmaceutical manufacturers face both opportunities and challenges to effectively support customers within these changing models in several key areas:

1. Prescribing Patterns and Drug Utilization: As practices consolidate, a more standardized approach to care emerges. Select networks are piloting treatment protocols and influencing prescribing patterns by specifying in-house experts to be consulted on specific disease areas or complex cases. Pharmaceutical manufacturers must be aware of these trends to engage effectively with these networks and ensure their products are included in future treatment guidelines and algorithms, the early foundations of which are already being developed at some practice groups. Payer utilization management remains a key factor in prescribing decisions. While some MSOs are exploring internal specialist committees and data-driven treatment guidelines, payer coverage policies and cumbersome prior authorization processes continue to shape which therapies gastroenterologists prescribe. This is particularly true for newer specialized and high-cost product types. Even with MSO support through dedicated prior authorization teams, providers cite difficulties in navigating payer coverage for desired regimens. This underscores the importance of understanding local payer dynamics when developing engagement strategies and deploying effective strategies to support the providers in mitigating significant payer coverage and reimbursement challenges.

“The whole idea is to have more influence to ensure better, quality patient care. As the alliance becomes stronger, we may have some more influence on payers and the prior authorization process”

-MSO Affiliated Gastroenterologist

2. Value-Based Care, Standardization & Quality: With MSOs capable of focusing more on value-based care, providers are incentivized to improve patient outcomes and reduce costs. By collaborating with large gastroenterology networks, manufacturers can demonstrate the effectiveness of their therapies in achieving better clinical outcomes and cost savings, increasing value recognition in the broader interests of MSOs. Increasingly, the use of generics and biosimilars, consideration of purchasing contracts, and formal value-based partnerships with payers will all inform practice network-level decisions.

3. Clinical Trials & Data Generation: With the consolidation of gastroenterology practices, networks have access to larger potential trial populations, creating attractive opportunities for clinical trial sites in collaboration with pharma. For example, GI Alliance offers robust clinical trial infrastructure across its practices, making it easier to recruit patients for studies. This reduces drug development timelines and enhances post-marketing surveillance, to help collect valuable real-world data on drug efficacy and safety. Larger networks also provide opportunities for pharmaceutical manufacturers to partner and collect data in new ways, providing valuable insight into the long-term effectiveness of therapies in diverse patient populations, which can support ongoing clinical research and long-term product value proposition, particularly in chronic disease areas with significant payer access burden, such as Crohn’s disease or ulcerative colitis. A future scenario could be considered where pharma companies collaborate with networks to generate real-world clinical and economic outcomes data, and then leverage data in interactions with payers to help alleviate coverage concerns for specialized and high-cost therapies.

4. The Evolving Pharma Strategy: The rise of MSOs and the breadth of their influence requires that pharmaceutical manufacturers adjust their engagement strategies. MSOs vary widely in their organizational structures, clinical focuses, and regional payer dynamics, but a general trend is the consolidation of “top-down” clinical and operational decision-making and emergence of population health decision-makers who will drive organization-level decisions bridging patient care with provider priorities and practice network sustainability. Decisions from these groups will impact across large numbers of practices, physicians, and patients. Pharmaceutical manufacturers will benefit from tailoring their engagement approach based on the specific needs of each MSO. Examples of tailored MSO engagement include working with specialist committees and new population health decision makers, aligning with value-based care goals, and navigating payer policies – all which can vary across different MSO groups. Recognizing these variations in MSO priorities can ensure more effective market penetration, drug adoption, and customer support.

Pharma Relationships with a Changing Gastroenterology Practice Sector

Private equity and management services organizations are reshaping the gastroenterology practice landscape. The increasing consolidation and internal transformation of practices, in context of novel treatments and payer utilization management, will collectively inform how pharmaceutical manufacturers approach this space. By building strong relationships with key stakeholders, aligning with new organizational goals, identifying MSO-specific regional payer interactions, and understanding drivers of prescribing and new drug adoption, pharma will be able to better support gastroenterology providers and patients.

Find out how The Dedham Group can support your gastroenterology practice outreach strategies. Contact us.

About the Authors

Kelsey Smart is a Consultant at The Dedham Group. Email her at [email protected].

Daniel Colacurcio is an Associate Partner at The Dedham Group. Email him at [email protected].

The post What Gastroenterology Practice Consolidation Means for Pharma Manufacturers appeared first on The Dedham Group.

]]>The post How Pathways Are Reshaping Community Oncology and Why Manufacturers Should Pay Attention appeared first on The Dedham Group.

]]>

Akshay Kamath, Daniel Colacurcio, and Sophia Tan

In 2024, the FDA issued over 60 oncology approvals, sustaining the high bar set by the agency in recent years. While encouraging, this influx of novel products and nuanced clinical data leaves generalist oncologists grappling with which regimens to keep in their treatment arsenal.

To help navigate this complexity, clinical pathways have stepped in to help standardize clinical decision-making across tumor types—reducing costs, integrating work-up guidance, and aligning with value-based care goals. Still, they remain costly, require dedicated personnel, and need frequent updates to remain relevant, making adoption challenging for smaller, resource-scarce community practices.

Despite these hurdles, pathways are gaining traction in community oncology. What’s driving this shift?

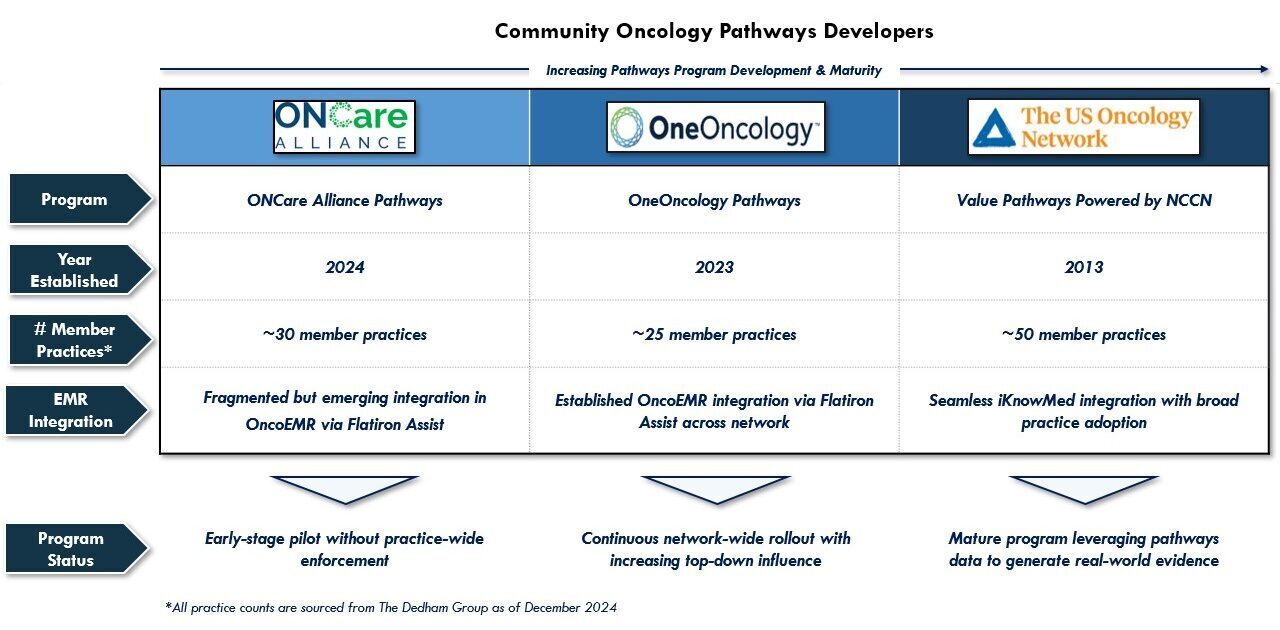

Practice Aggregators: A Catalyst for Pathways Adoption

In the past year, practice aggregators such as OneOncology have fueled the growing exposure of pathways in community oncology, rapidly acquiring oncology clinics and standardizing decision support tools across their networks. Pathways have become one of those critical tools to ensure clinical consistency, improve quality metrics, and strengthen contract negotiations, allowing aggregators to exert greater top-down control over treatment decisions. Over time, members of these aggregators have transitioned to standardized EMRs, piloted aggregators’ pathways in key indications, and, in some cases, promoted pathways adherence via incentives and penalties. Yet, the evolution of pathways within aggregators remains diverse, shaped by varying levels of practice autonomy and differing standardization priorities, as seen in the chart below.

As these unique practice aggregator models continue their expansion across independent practices, it follows that their pathways programs will remain a strategic element supporting new therapy adoption, biomarker testing visibility, and top-down clinical standardization, foreshadowing their potential to become evidence-generation engines.

Beyond Aggregators: Other Forces Driving Pathways Adoption in Practices

While practice aggregators will likely continue to be the largest source of pathways activation in the community setting, other forces may also accelerate their adoption in the coming years:

- Growing Academically-Developed Pathways Interest: Large, elite academic centers, such as Dana-Farber Cancer Institute, are leveraging their sphere of influence to expand pathways reach to select practices, shaping decision-making beyond their institution.

- Greater Customizable Platform Options: Platforms such as Flatiron Assist provide NCCN-based pathways templates, and while building and maintaining a pathways program is no small investment, this makes it simpler for community accounts to build their own internal pathways solutions and shift existing content from loose PDF-based formats to user-friendly, scalable systems.

- Increasing Provider Consolidation: Naturally, mergers and acquisitions of oncology practices has driven the harmonization of clinical decision-support tools, in many cases resulting in the acquired entity adopting pathways from the absorbing entity.

- Expansion Into Adjacent Specialties: Oncology pathways are making inroads into therapeutically-adjacent community clinics. Specifically, urology practices are just beginning to build in oncology pathways, among other access levers, to assist with prescribing standardization.

Pathways Alternatives

Not all community oncology practices have the resources or support to invest in full-fledged pathways programs, but many are exploring alternative models that offer standardization without the heavy lift:

- Payer Pathways Integration: Some practices are embedding existing payer pathways recommendations into their EMR workflow. One community practice piloted an approach where their EMR surfaced UHC Cancer Therapy Pathways recommendations at the top of the treatment selection screen, allowing HCPs to more naturally select preferred regimens without imposing strict adherence requirements. This approach enabled them to test buy-in, attain financial incentives and electronic prior authorizations from UHC, and avoid costly EMR transitions.

- “Pseudo”-Pathways Users: In lieu of formal pathways, some practices use preferred regimen lists or sophisticated formularies to drive evidence-based, cost-effective prescribing while avoiding the operational burden of pathways governance. Although these models may lack the same line of therapy or biomarker specificity as traditional pathways, they permit increased scrutiny on product use in priority classes, helping monitor clinical variation without nearing the infrastructural lift of a formal program.

- AI-Driven Decision Support Systems: Emerging AI-driven clinical decision support tools may increasingly fill the gap for practices that want the insights of a pathways program without the rigidity of a formal program. Companies like Tempus have been developing machine learning algorithms to pinpoint deviations from care guidelines in select tumor types, serving a dynamic role in minimizing prescribing variation without significant practice-level overhauls.

As practices continue to consolidate, these alternative models may also gain traction and should not be overlooked in a holistic engagement strategy.

Why This Matters for Manufacturers

Ultimately, pathways adoption in the community is growing but remains fragmented, shaped by varying developer models, standardization philosophies, and degrees of implementation. For manufacturers, this presents both a challenge and an opportunity. Successfully engaging in the pathways channel requires a nuanced understanding of who these groups are, how they influence prescribing patterns across a growing user base, and how they are uniquely positioned to evolve in the coming years.

Pathways offer a direct line to large networks of affiliated community oncologists, alongside a new generation of system-level, cross-functional decision-makers, making them a powerful channel for amplifying new clinical data. However, engagement must be executed tactfully and with an acute awareness of program-level decision-making drivers.

As standardization efforts continue, manufacturer teams that proactively navigate this landscape can better position their therapies for adoption in community oncology.

Find out how The Dedham Group’s expertise can improve your pathways strategies. Contact us.

About the Authors

Akshay Kamath is a Principal at The Dedham Group. E-mail him at [email protected].

Daniel Colacurcio is an Associate Partner at The Dedham Group. E-mail him at [email protected].

Sophia Tan is a Managing Partner at The Dedham Group. E-mail her at [email protected].

The post How Pathways Are Reshaping Community Oncology and Why Manufacturers Should Pay Attention appeared first on The Dedham Group.

]]>The post How Healthcare Systems Can Support Cell and Gene Therapy Growth appeared first on The Dedham Group.

]]>

By Kian Talaei, Senior Consultant

With the rapid increase in approvals for cell and gene therapy (CGT) products, a critical question emerges: does our healthcare system have the capacity to meet the growing patient demand? The CGT pipeline is continually expanding, with nearly 3,000 assets in development from preclinical through pre-registration phases, according to a report from ASGCT and our sister company, Citeline.

As more cell and gene therapies transition from clinical trials to commercially available product, there will be a need for healthcare providers to accommodate rising patient volumes. Healthcare providers will need to strategically expand capacity or develop new capabilities to address demand.

Pharmaceutical companies can play a role in ensuring adequate capacity is available to meet demand. Understanding influences on site capacity can enable development of forward-looking strategies to optimize patient reach.

Key Factors Impacting Healthcare System’s Cell and Gene Therapy Capacity

The ability of healthcare systems to support CGT growth depends on a range of internal and external factors:

Internal Capacity Factors

- Patient Identification, Referral, and Care Coordination: Delayed identification, referral and medical information sharing for CGT-eligible patients can contribute to provider site inefficiencies in scheduling and resource allocation. Delays are often driven by low awareness of CGT options, prioritization of alternative options available on-site, unestablished referral protocols, and mismatched or incompatible EHR systems between provider sites.

- Infrastructure Limitations: Availability and allocation of physical infrastructure limits provider sites’ ability to treat the full CGT-eligible population. Sources of capacity bottlenecks include availability of inpatient beds, apheresis slots, surgical space, cell processing capacity and dewar/storage space, and are often exacerbated by unpredictable patient flows and referral inefficiencies.

- Department-Level Bottlenecks: Many commercially available CGTs, particularly within the oncology space, are managed by a hospital’s bone marrow transplant (BMT) team. If BMT departments continue to be prioritized for CGT volume, the time and resources needed can exceed existing physician and supporting staff availability.

- Availability of Skilled Staff: Specialized staff, including nurses and apheresis teams, are essential for CGT administration. However, high turnover rates, nuanced training requirements, and the need for specialized 24/7 AE monitoring may limit the number of patients that healthcare centers can support.

- Financial Feasibility of Expansion: Many healthcare sites, especially smaller community-based hospitals and practices, face cash flow constraints due to the high upfront costs of CGT treatments (ranging from half a million to over $3 million per patient). Many smaller hospitals may not be able support higher CGT patient volumes while maintaining financial sustainability, driven by credit limit caps, risks of insufficient payer reimbursement (e.g., Medicare FFS, Medicaid), and extended times to reimbursement (e.g., 30-120+ days post-treatment).

External Capacity Factors

- Slot Availability and Manufacturing Timelines: Slot availability and production timelines requires agile site flexibility in patient scheduling and CGT administration. This limits provider sites’ ability to operate at full capacity or results in rescheduling patients with less urgency to treat (e.g., pushing back infusion date).

- Administrative Burden of Payer Approvals per CGT Case: Market precedent has shown that in the first year of launch, it can take several weeks to months to obtain full coverage for each CGT patient case, partly due to cost scrutiny (e.g. prior authorizations, peer-to-peer reviews, appeals, single case agreements for reimbursement). This places more administrative burden on the provider site than standard therapeutics. As CGT cases increase, provider sites will face greater administrative capacity constraints.

- Availability of Essential Supporting Drugs: Select drugs (e.g., fludarabine, tocilizumab, etc.) are essential for supporting CGT treatment. Shortages in these drugs due to manufacturing & supply chain disruptions, regulatory barriers, and increased global demand may have downstream effects on the ability for provider sites to appropriately treat CGT patients.

Opportunities to Minimize Capacity-Driven Barriers to CGT Utilization

As CGT continues to evolve, addressing these capacity challenges is essential to ensuring patient access to life-saving treatments. Pharmaceutical manufacturers, healthcare providers, and policymakers must collaborate to build scalable, efficient, and financially sustainable models for CGT growth.

Pharmaceutical companies can help enable the availability of capacity to meet product demand with strategic planning and cross-industry engagement. While some solutions require national-level policy adjustments, such as improving reimbursement structures and expanding workforce training programs, others can be achieved with provider site mix optimization and partnership. Potential near-term solutions may include, but are not limited to:

- Considering capacity in provider site selection for activation

- Establishing CGT referral networks and protocols from community sites

- Partnering with provider sites on best practices for capacity optimization (e.g., outpatient administration, scheduling coordination, staff and physical resource allocation)

- Supporting provider sites in diversifying CGT staff from traditional oncology/BMT departments with staff training and protocol templates

By addressing these capacity influences proactively, we can enhance accessibility and ensure that more patients benefit from these transformative therapies.

Find out how The Dedham Group’s expertise can enhance your cell and gene therapy strategies. Contact us.

The post How Healthcare Systems Can Support Cell and Gene Therapy Growth appeared first on The Dedham Group.

]]>The post Four Strategies for Competing in the Crowded Obesity Drug Marketplace appeared first on The Dedham Group.

]]>

By Manny Jurado, Associate Partner

Over 100 million Americans are classified as medically overweight, making obesity one of the fastest growing public health issues in the U.S. The anti-obesity medication (AOM) marketplace is rapidly expanding, with analysts estimating it to be worth $150 billion by 2032, fueled by the increasing demand for effective weight management (e.g., 15-25% weight loss) and metabolic health solutions. With potential Medicare coverage on the horizon and increasing patient demand, the obesity space promises to grow at an unprecedented rate.

The obesity space is burgeoning with significant competitive intensity, as numerous manufacturers invest into additional clinical pipeline assets, increasing the need to differentiate within the frantically evolving space. The diagram below illustrates a current snapshot of the intense competition in the weight loss landscape:

Visual Credit: Sophia Rawson, Chike Onyia, Nicholas Colaw

As the AOM market continues to grow, manufacturers must navigate a range of critical market dynamics, including emerging access dynamics, clinical differentiation needs, patient access challenges, and emerging opportunities for partnerships. These factors underscore the need for proactive strategies that capitalize on opportunities and mitigate potential barriers, to optimize future product market share and maintain a competitive edge.

Here are four strategies to stand out in this dynamic landscape:

1. Leverage Emerging Pathways for Access

Manufacturers must adapt and respond to increasing budget impact pressure for key access stakeholders and potential therapy restrictions implemented by emerging PBM/ coverage models.

Employer Coverage Trends

As a new stakeholder in the commercial space with decision making power, employers wield significant influence over GLP-1 coverage decisions. As the new calendar year unfolds, many employers are reassessing coverage options, balancing the potential benefits of improved employee health and satisfaction against their concern for budget impact due to the high cost of GLP-1s.

Education on GLP-1s and their benefit to employers may help shape future coverage decisions. Companies like Novo Nordisk and Eli Lilly are already engaging directly with employers, providing clinical value story evidence and cost-effectiveness data to support coverage decisions.

Alternative AOM Coverage Programs

The rise of carve-out programs and alternative PBM (pharmacy benefit manager; e.g., CapitalRx, Rightway, Waltz Health) models reflect the need for greater transparency in managing AOM coverage. These models enable employers and health plans to opt into AOM coverage with potential customized guardrails (e.g., restrictive HCP network, value-based milestones, pre-GLP-1 requirements). Most importantly, they offer higher levels of price predictability, rebate visibility, and spend transparency over time.

These are all important factors that enable those at-risk for pharmacy spend to gather more data to inform decisions and implement strategies to enable GLP-1 coverage. By understanding future PBM disruptors, manufacturers can better prepare messaging around optimized cost predictability and patient outcomes. Manufacturers could also benefit from monitoring restrictions and identifying alignment to GLP-1 clinical value story, while keeping eyes open for partnership opportunities.

Point Solutions

Select PBMs and employers provide digital health services such as point solutions (e.g., Vida Health, OptumRx Weight Management Program) that serve as a preliminary step to accessing AOMs. These programs often require patients to first complete a structured weight management program offered through the PBM before being approved for GLP-1 treatments, in an attempt to align clinical treatment with cost-effectiveness goals. Manufacturers may combat access restrictions through education on how concurrent solutions may be more beneficial to patients, emphasizing data in support of an initial synergistic therapy approach.

2. Identify Areas for Clinical Differentiation

To stand out clinically amidst increasing competition, manufacturers are moving beyond weight loss to explore expanding indications, novel clinical pathways, and additional therapeutic benefits. Exploring these alternative methods opens the door for potential key clinical differentiation from competitors.

Novel Indications

Trials are underway to assess GLP-1 efficacy in areas such as sleep apnea, cardiovascular risk reduction, neurodegenerative diseases (e.g., Alzheimer’s, Parkinson’s), and women’s health conditions like PCOS. Demonstrating improved outcomes across these diverse conditions could significantly enhance a product’s value proposition and improve opportunity for coverage.

Specific Outcomes

Even within weight loss, manufacturers have an opportunity to highlight more targeted outcomes, including preservation of lean muscle mass (emphasizing fat loss over muscle loss is critical, particularly for vulnerable populations like the elderly). Exploring mechanisms to prevent rebound weight gain after discontinuing therapy could also further differentiate products.

Emerging ROAs

Traditional injectable GLP-1 therapies are being complemented by oral and potentially sublingual formulations. These innovations aim to improve patient adherence and convenience, which could increase clinical value to patients.

Unique MOAs & Combinations

To achieve these unique outcomes, manufacturers are investigating novel mechanisms of action (MOAs) to target weight loss via multiple metabolic pathways. Trials assessing combinations of GLP-1 agents with GIP agonists and/or GCGR antagonists have proven to effectively produce both significant weight loss results and improvements in adjacent therapeutic areas. Leveraging the proven efficacy of current treatments with these new pathways may prove to be a lucrative value offering for manufacturers looking to stand out.

Regulatory Considerations

Under specific FDA regulations, particularly during shortages, compounding pharmacies can produce non-identical versions of GLP-1 drugs, such as semaglutide and liraglutide. While this supports patient access, compounded therapies threaten the clinical value story of FDA-approved weight-loss therapies.

Manufacturers can differentiate from compounds with a distinct edge by highlighting safety concerns and regulatory differences. Compounded drugs often lack the rigorous quality control mandated for FDA-approved products. Counterfeit versions of branded drugs with harmful or inactive ingredients further exacerbate risks. Manufacturers should continue to highlight the safety and efficacy of FDA-approved products in their marketing efforts, emphasizing adherence to stringent regulatory standards. This strategy not only reassures patients but also aligns with broader advocacy efforts, such as Novo Nordisk’s and Eli Lilly’s petitions against unsafe compounding practices.

3. Optimize Patient Access

Manufacturers can gain an upper hand in market access differentiation by streamlining patient access to GLP-1s and draw in the AOM market by providing increased convenience and patient affordability. To compete effectively, there are a variety of approaches manufacturers may take to ensure patients can easily access their therapies.

Direct-to-Patient Platforms

Companies like Pfizer and Lilly are already leading the way with online programs that connect patients to telemedicine providers for streamlined access to treatment. These direct-to-patent platforms bypass the challenges of traditional in-person HCP visits such as appointment availability and travel, making at-home care easier. Bolt-on affordability solutions (e.g., copay cards, cash options) can further enhance financial accessibility to these therapies for patients.

Alternative Care Channels

Partnerships with medical spas and wellness centers present new avenues for distribution, expanding reach beyond traditional healthcare settings. These alternative care channels may attract new patients, and some locations are staffed with in-house MDs to prescribe and order GLP-1s efficiently.

PCP Channel Activation

Ongoing education and familiarization of primary care providers on the efficacy and appropriate utilization of GLP-1s is critical to market access pull-through, given that a great majority of GLP-1 prescriptions originate from the PCP channel.

4. Partner with Novel Supportive Technologies

Given the emergence and increased adoption of digital health in the U.S., collaborations with digital healthcare companies may enable manufacturers to offer surround-sound solutions that support enhanced clinical outcomes and the overall patient experience.

Digital Companion Apps

Non-regulated digital therapeutic tools (e.g., Livongo, Noom, Medisafe) can serve as valuable adjuncts to traditional pharmacotherapies, enhancing chronic condition management and driving improved patient outcomes. These digital solutions enable continuous patient monitoring, real-world data (RWD) collection, and follow-up engagement, which all serve to strengthen clinical development efforts. Additionally, personalized behavioral support features—such as cognitive behavioral therapy, live weight management coaching, symptom/side-effect tracking, and fitness/nutrition guidance—offer a more holistic approach to obesity and metabolic disease management, ultimately improving adherence and long-term success.

Combo Prescription Digital Therapeutics (PDTs)

Unlike traditional companion apps, combo PDTs undergo parallel clinical trials alongside pharmacotherapies, offering a rigorous, data-backed pathway to regulatory approval. These integrated digital solutions unlock greater clinical label expansion opportunities by increasing real-world evidence generation and product differentiation. Additionally, PDTs enable customized patient engagement strategies, such as drug-specific education and adverse event support, ensuring patients remain engaged throughout their treatment journey. As the U.S. healthcare landscape evolves, manufacturers who integrate PDTs into their market access strategy stand to gain a competitive advantage by aligning with evidence-driven, outcomes-based care models.

Emerging Third Party Technology: AI-Enabled Predictive Modeling, EMR Data Mining

New solutions such as EMR & AI technology continue to emerge within the healthcare space as tools that enable manufacturers to enhance their market offerings. As the bar for coverage and value of data heightens, opportunities emerge for solutions that enhance innovation within the obesity patient paradigm. An AI solution may be implemented to identify and predict current and future patients, improve clinical outcomes, or enhance transparency/predictability within the patient journey.

Additionally, manufacturers may consider working with sophisticated EMR vendors to implement internal flags or capture novel data sources that could facilitate brand growth through evidence generation. This could also support alignment to a future focus in value-based care, by increasing ease of execution for risk-based agreements. As opportunities continue to arise and develop, manufacturers can stay a step ahead through creative ideation and implementation of novel tools and unique partnerships.

Key takeaways from strategies to succeed in the obesity market:

- Monitor the evolving access landscape

- Identify high-value partnerships

- Develop novel HCP strategies

- Secure clinical and market access strategy differentiation

As the healthcare landscape evolves, successful strategies will depend on a data-driven understanding of key adoption trends, access stakeholder priorities (e.g., payer, employer, PBMs), and high-impact technological areas. This will empower manufacturers to proactively address market challenges, enhance product positioning, and maximize access success.

The AOM marketplace presents unparalleled opportunities for pharma manufacturers willing to innovate and differentiate. By expanding therapeutic benefits, improving access, and embracing digital and strategic partnerships, companies can secure their position in this crowded yet promising field.

Find out how The Dedham Group can help you navigate AOM strategies to stand out in the marketplace. Contact us.

The post Four Strategies for Competing in the Crowded Obesity Drug Marketplace appeared first on The Dedham Group.

]]>