The post A 1990s Playbook for 2025: What John Malone and the Telecom Era Can Teach Us about AI Infrastructure appeared first on Point72 Ventures.

]]>A question I hear over and over in venture circles right now: is AI ushering in a real transformation? Or are we repeating the telecom bubble of the 1990s?

This summer, I picked up John Malone’s new autobiography, Born to Be Wired. Through Liberty Media, Malone backed iconic consumer brands like Formula 1 [3], SiriusXM [4], and Live Nation [5], and also held positions in Expedia [6] and QVC [7]—proving his eye for durable, consumer-facing businesses.

But his career-defining move came much earlier. During the telecom boom of the 1990s, he scaled and sold Tele-Communications Inc. (TCI)—then one of the largest cable providers in the U.S.—to AT&T for $48 billion [9], in a deal that many now see as a parallel to today’s AI buildout.

I was expecting some good media anecdotes. What I got instead was a masterclass in how to think about infrastructure, consumer pull, and capital strategy—three themes that feel eerily relevant to what I think we’re seeing in AI today. I had personal reasons for picking it up: Malone grew up in Milford, Connecticut, just 10 minutes from where I did [1]. He also went to Yale, where I studied as well [2]. But the deeper resonance came from his approach to building in uncertain environments.

Malone’s story reminds us: just because something looks like a bubble doesn’t necessarily mean it is. And more importantly, even bubbles can leave behind infrastructure that powers generational companies—if those companies are built with the right mix of vision, discipline, and creativity. Here are the most important lessons I think founders can take from Malone’s story:

Bet on Infrastructure, But Pressure-Test the Demand

John Malone was a man who saw around corners. Long before “broadband” was a buzzword, he envisioned cable as the “information superhighway” [10], a vast network capable of delivering far more than just television.

But the high costs of set-top boxes (up to $7,000 each) and the complexity of early interactive TV meant business models didn’t deliver immediate ROI [14]. Yet Malone didn’t pull back. Instead, he stuck with his vision, betting that the infrastructure he was building would eventually become indispensable. He was right. The same fiber-optic pipes once dismissed as failures became the foundation for broadband internet and made today’s platforms like YouTube and Facebook possible [12].

The idea that killer applications can come years later is one our team talks about often when speaking with AI infrastructure companies with AI infrastructure companies. Right now, everyone seems to be focused on compute, GPUs, and model architecture. The capital going into this space is enormous, and the obvious question is: are we investing ahead of sustainable demand, or just chasing a moment?

Malone’s mentor, Monty Shapiro, had a mantra that stuck with him: “What if not?” [13] What if the consumer use case never comes? What if the ROI isn’t immediate? That lens—optimism tempered with scenario planning—is something I believe founders should adopt today. Especially those building deep tech foundations.

The cautionary tale here is Nortel. In the 1990s, Nortel’s revenue ballooned in part because it was financing its customers’ purchases. It was a short-term win that unraveled when demand didn’t materialize. Today, as Nvidia sells record volumes of chips, I think it’s fair to ask: are we seeing similar dynamics? And if so, how do we make sure we’re building something that lasts beyond the hype?

Only Real Demand Justifies AI’s Infrastructure Spend

There’s a lot of dazzling AI content out there—viral Drake songs, anime-style art, hyperreal videos—but in my opinion many of these tools still feel like tech demos. What’s the consumer hook that keeps them coming back? That’s the question that I think matters.

Malone understood this intuitively. He didn’t just invest in cable infrastructure, he backed HBO, CNN, MTV, BET [18]. Because he knew what actually drove growth was content people cared about. He believed distribution only mattered if you had something worth distributing.

As I read the book, I saw parallels to some of the ways our portfolio companies are playing in the AI sphere:

- Fever uses AI to match consumers with live experiences they’ll love—and does so in a way that feels invisible, seamless, and consumer-first. This is a direct application of Malone’s consumer-driven philosophy to the experiential economy.

- GlobalComix applies AI translation to make global comics accessible to more readers. It’s not about the AI—it’s about unlocking demand. This reactive approach, exemplified by their partnership with Marvel, demonstrates how AI can unlock and expand the reach of beloved content.

- Range Media Partners puts talent at the center, and sees AI as a tool to amplify creators, not replace them. That mindset is critical. Whether it’s a blockbuster film or a compelling series, the core appeal of a well-told story remains paramount, and AI can serve as an invaluable co-pilot in its creation and distribution, not a replacement for its essence.

In each of these cases, I believe the tech only matters because it solves a real problem. If you’re a founder in AI media or consumer, the bar isn’t novelty, it’s staying power. I think you should ask yourself: would a user still care about this six months from now?

Modern Consumer Startups Need Modern Financing Models

I used to structure equity derivatives at Goldman Sachs. Back then, John Malone’s name came up constantly. Not just because of what he built, but how he financed it. He made cable work in a capital-intensive environment by inventing new ways to deploy it: spin-offs [21], tracking stocks, tax-advantaged swaps [22]. EBITDA as a metric was practically weaponized [20].

Consumer companies today are running into their own capital constraints, but the dynamics are different than they were for John Malone. Most aren’t spending on infrastructure; they’re spending on customer acquisition. And equity financing isn’t always the right tool, especially when founders want to protect ownership.

That’s why we’re excited about the rise of UA financing and revenue-based funding. As John Malone did with EBITDA, we’re excited to see the consumer startup industry rethinking growth investment strategies. When the payback math works, I think there’s no reason not to at least consider financing with non-dilutive capital.

Our portfolio company Ladder is a great example. They recently raised UA financing from General Catalyst that allows them to scale without giving up equity. That’s a Malone-style move—structuring capital to match the business model.

I believe founders should be thinking this way: how do you fund growth without mortgaging the future? I think that’s what creative capital allocation is really about.

Build for the Long Game, Grounded in Demand

John Malone’s story is more than a telecom history lesson. It’s a roadmap. For AI founders, I believe the path forward isn’t just about building fast. It’s about building right. That means:

- Being patient enough to bet on infrastructure that won’t pay off right away

- Staying grounded in what consumers actually want

- Finding smart, flexible ways to finance growth

If you’re building in AI infrastructure, media, or consumer experiences and wrestling with the same “What If Not?” questions, let’s talk: [email protected].

Footnotes

- John Malone, Born to Be Wired: Lessons from a Lifetime Transforming Television, Wiring America for the Internet, and Growing Formula One, Discovery, SiriusXM, and the Atlanta Braves (Simon & Schuster, 2025), 17. [

]

] - Malone, Born to Be Wired, 29. []

- Malone, Born to Be Wired, 329, 334-335. []

- Malone, Born to Be Wired, 291-292, 296-299. []

- Malone, Born to Be Wired, 280-281, 288-289. []

- Malone, Born to Be Wired, 272, 275, 283. []

- Malone, Born to Be Wired, 93, 103, 151, 275, 277. []

- Malone, Born to Be Wired, 12, 59-60, 243, 341. []

- Malone, Born to Be Wired, 241. []

- Malone, Born to Be Wired, 139. []

- Malone, Born to Be Wired, 71, 139, 147. []

- Malone, Born to Be Wired, 16, 71, 179, 386-387. []

- Malone, Born to Be Wired, 14, 43. []

- Malone, Born to Be Wired, 65, 139-140, 158. []

- Malone, Born to Be Wired, 51. []

- Malone, Born to Be Wired, 99, 152. []

- Malone, Born to Be Wired, 99, 112, 115. []

- Malone, Born to Be Wired, 59-60. []

- Malone, Born to Be Wired, 120-123. []

- Malone, Born to Be Wired, 244, 339-341. []

- Malone, Born to Be Wired, 66, 77, 79. []

The post A 1990s Playbook for 2025: What John Malone and the Telecom Era Can Teach Us about AI Infrastructure appeared first on Point72 Ventures.

]]>The post Our Investment in Heidi Health appeared first on Point72 Ventures.

]]>

We are excited to announce that Point72 Private Investments is leading a $65 million Series B in Heidi Health, an AI-powered clinical documentation platform focused on reducing the administrative burden on clinicians.

Clinical documentation is essential to delivering safe, coordinated care and securing reimbursement, yet, in our view, it remains one of healthcare’s most persistent pain points. A 2022 study found that clinicians spent an average of 13.5 hours per week on documentation – a significant burden that frequently spills into personal time.

Heidi seeks to address what it sees an unhealthy dynamic where clinicians often find themselves hunched over laptops during patient visits, typing notes, and later spending additional hours between appointments or after-hours refining documentation, which can exacerbate clinician burnout, reduce meaningful patient interaction, and ultimately diminish healthcare system capacity.

Heidi is seeking to tackle this problem head on by reimagining documentation processes through AI. The team builds from a deep conviction that accurate clinical transcription is the critical foundation for true healthcare automation. By capturing medical encounters in precise detail, Heidi’s platform aims to be the key that unlocks the automation of complex workflows – from care coordination to revenue cycle management – and to lay the groundwork for products that could transform how care is delivered.

Heidi has experienced impressive results. In just 18 months, Heidi has returned more than 18 million clinical hours to frontline caregivers and now supports over 2 million patient consults weekly across 116 countries and 110 languages, demonstrating both the urgency of the problem and the effectiveness of Heidi’s approach.

Heidi is designed to work alongside clinicians in every patient interaction, capturing the conversation in real time and automatically producing structured, high‑quality clinical notes. The goal is that clinicians can stay present with patients during consultations while ensuring comprehensive documentation is ready the moment the visit ends, eliminating the need to type during the appointment or spend nights refining notes.

From there, Heidi offers clinicians tools to customize their workflows with specialty‑specific templates and share them with Heidi’s global community. This collaborative approach has created a growing library of best‑practice templates, now used by thousands of clinicians worldwide. By standardizing high‑quality documentation at the specialty level, Heidi’s goal is that these templates will reduce review time and help avoid costly errors.

Beyond documentation, Heidi’s AI capabilities aim to address the broader administrative workflow:

- Ask Heidi uses natural language prompts to trigger follow‑up tasks or generate additional documents.

- Task‑list automation offers care teams tools to coordinate on next steps without manual tracking.

- Clinical coding works to translate documentation into billable codes to improve reimbursement efficiency.

- Calls can be used to automate routine patient outreach for check‑ins and reminders to keeping patients connected to their care between visits.

Heidi’s work to streamline these processes is in service of its mission to return precious hours to clinicians, help prevent burnout, and improve the patient experience, all without sacrificing accuracy or compliance. It means that every clinician is practicing with an AI partner in care.

Heidi’s goal is for clinicians to experience dramatically reduced documentation time, lighter cognitive load, and newfound ability to maintain work-life balance, allowing the doctors to focus on their patients rather than screens. Users have exhibited consumer-like engagement metrics on Heidi’s platform, suggesting the platform is integral to their daily workflow.

When we first met Tom, Waleed, and Yu, we were impressed by their single-minded focus on serving clinician end-users. From our first meeting, we saw a sense of urgency driven by lived clinical experience and a relentless focus on progress. Tom, a former clinician who built Heidi based on his own experience with excessive paperwork, brings what we see as valuable customer empathy to how the company approaches platform development.

What stood out to us was the combination of the traction that the team had already achieved and their vision for what comes next. Heidi has attracted customers ranging from solo practitioners to some of the world’s largest health systems.

Our investment in Heidi builds on our broader healthcare AI thesis. When we invested in Adonis last year, we believed that AI-powered automation could narrow the gap between healthcare cost and quality, driving meaningful improvements to patient outcomes and economics globally. Our partnership with Heidi continues this thesis.

We are proud to support Heidi Health’s mission to provide meaningful relief for the clinicians at the heart of our healthcare system, giving them more time and energy to focus on what matters most: delivering better patient care.

The post Our Investment in Heidi Health appeared first on Point72 Ventures.

]]>The post Inside the Consumer Health Renaissance: Navigating Personalized Wellness in a Shifting Landscape appeared first on Point72 Ventures.

]]>Over the past few years, we’ve observed consumer health evolve from a niche category into something that feels fundamental. It’s no longer just “wellness” on the fringe—it’s a $6.3 trillion global economy, including a $2.2 trillion U.S. market. And from what we’re seeing, it’s still expanding, driven by changing consumer expectations and increasingly accessible technology.

What we might have once thought was reactive and physician-led now appears to be proactive and consumer-directed. Supplements, wearables, diagnostics and treatments that were once considered luxury goods or niche tools are seemingly commonplace. I’m seeing today’s consumers increasingly prioritize solutions that help them feel better, look better and live longer—and that they’re willing to invest in what works. Even, it turns out, in a down market.

So where are we today? I’d describe this as a pivotal moment: one where foundational consumer behaviors are colliding with emerging tech to redefine what “health” means on a personal level.

The Shifts We’re Watching Closely

Several converging factors are changing the shape of how we think about the consumer health landscape. Some dynamics we find particularly compelling:

1. The GLP-1 Effect

The rise of GLP-1s (Ozempic, Wegovy, Mounjaro) has been a cultural and clinical tipping point, with 1 in 8 U.S. adults using these medications in 2024. I see this as an indicator that when a solution is both effective and relatively frictionless, adoption can often follow. More broadly, this may also be a signal on how demand is shifting across adjacent categories, which are now being re-evaluated through this new lens.

Some surgeons report that about 20% of their new cosmetic patients are GLP-1 users, often interested in skin tightening after rapid weight loss. In the food and beverage sector, households with GLP-1 users have cut their grocery and dining spend by about 6% and demand has shifted toward more “functional” nutrition such as high-protein snacks and low-sugar options. Users are also looking for ways to preserve muscle mass, fueling demand for protein supplements, strength training and recovery services. Finally, a growing number of wellness platforms are integrating GLP-1 programs, signaling that clinical interventions are becoming part of mainstream consumer health.

2. Information Overload

Social media is a powerful discovery engine, with 39% of consumers buying wellness products from influencer recommendations. But this can also increase information overload and misinformation. Just one recent, personal example: I searched for a specific recovery tool for an ankle injury and was suddenly served over 20 related products across each of my social media accounts. Meanwhile, it feels like a single health-related TikTok trend can go viral overnight with users contributing their own takes, regardless of their credentials.

3. From Manual to Passive Tracking

Nearly 1 in 3 Americans now use a health-tracking device, and we’re seeing a shift from manual logging of meals, workouts and sleep toward continuous, automated data capture. I think one of the most exciting shifts in consumer health is how passive tracking has become. With wearables, at-home diagnostic, and AI-powered platforms, people no longer have to log every meal or workout manually. The data flows from the wearable. I’ve explored some platforms that offer over 100 biomarker panels, which to me signals how much deeper consumer curiosity is getting. And with daily feedback from continuous monitoring, health insights are becoming more immediate, more personal, and from my perspective, more useful than ever before.

In parallel, interoperability standards such as Apple HealthKit, Google Health Connect and FHIR APIs are enabling fitness, lab and nutrition data to flow between platforms. Together, we see these shifts pointing to a consumer health experience that is becoming more connected, automated and personalized.

4. Aesthetics and Measurable Outcomes Matter

In my view, visible and tangible progress is one of the most underrated motivators in consumer health. Whether it’s clearer skin, improved body composition, or better sleep metrics, I think people are simply more likely to stick with routines when they can see that something is working. It’s not vanity — it’s basic psychology. Measurable results tend to reinforce behavior, and in a world flooded with wellness choices, outcomes are often what make something worth continuing.

Studies suggest that appearance-linked confidence can motivate consistent health behaviors like gym attendance and following dietary plans. The key, we believe, is blending functional health with aesthetic results for improvements that are both seen and felt.

Where We See Opportunities for Founders

As a team, we’re actively thinking about how companies can best serve this evolving consumer. Some of the areas we’re particularly excited about include:

Building Around GLP-1 Ripple Effects

As more people experience weight loss, we expect to see continued demand across the categories mentioned above: skin tightening and cosmetic procedures, muscle preservation and performance, high-protein snacks and supplements. We believe the winners won’t just be the drugs themselves, but the ecosystem builders—the products and services that help consumers navigate new bodies, new routines and new needs.

Trusted Distribution Models

In-app shopping features make it easier than ever to buy products without leaving your social platform of choice. Just one example: 43.8% of TikTok users made a purchase from the platform’s shop in 2024 and 79.3% of TikTok Shop sales in the U.S. are health and beauty products.

Meanwhile, a single trend like #GutHealth on TikTok can generate billions of views in a matter of weeks. But the same dynamics that drive discovery can also accelerate misinformation. In this environment, trust is a critical factor: 52% of US adults and 77% of Gen Z use social media as a trusted source for beauty and personal care information. Surveys indicate that more than half of consumers consider recommendations from health experts to be their most reliable source when making wellness purchases. This suggests an opportunity for platforms that help reduce noise by guiding consumers toward evidence-backed solutions, and for models that enable practitioners and experts to play a larger role in the consumer discovery process.

Simplification through Integration

To me, one of the biggest pain points in consumer health right now is just how fragmented the ecosystem still is. You’ve got wearables over here, supplements over there, diagnostics in one portal, coaching in another. Consumers I’ve spoken to end up juggling multiple apps, devices, and dashboards with no single source of truth. It’s not for lack of innovation, it’s just that none of it talks to each other. From our perspective, the most defensible solutions will likely be those that lower friction and create continuity across different aspects of the health journey, reducing cognitive load and making the experience feel integrated, not scattered.

Diagnostics as a Consumer Product

I think one of the subtle-but-important shifts in consumer health is how diagnostics have moved beyond the doctor’s office. What used to be physician-gated can now be a direct-to-consumer experience—accessible, even aspirational. We’re seeing lab tests rebranded into tools for self-optimization, tapping into what I’d call “health curiosity” as a cultural norm. But here’s our perspective on the catch: We believe that data alone isn’t enough. Without utility—coaching, guided behavior, personalized insights—it’s likely just noise. In my view, the stickiest platforms are the ones that make diagnostics feel as habitual and actionable as checking your bank account or tracking your daily steps.

Behavioral Design

In my experience, access to health data is no longer the problem. It’s what people actually do with it that matters. Meaningful results are still hard to achieve, and long-term retention often hinges on whether a product becomes second nature. The best platforms I’ve seen don’t just deliver data but aim to create habits. Whether it’s visible progress tracking, social accountability or gamified streaks, these small design choices can make a huge difference. I’m also seeing community playing a big role. People stick with routines when they feel supported. Personally, I think the most effective consumer health experiences are the ones that blend behavioral science—like habit formation and motivation—with biology, translating metrics into something people can actually see and feel.

Clinical efficacy = differentiation

In my view, clean ingredients and transparency are just the starting point for today’s consumer, not the finish line. People are more discerning than ever when it comes to health and wellness purchases. Whether it’s a protein bar, supplement, device or diagnostic, they want evidence that it actually works. I’ve personally seen countless brands with strong marketing fail to get traction because they lacked scientific credibility. Especially in crowded categories like personal care and supplements, I believe that science-backed, proprietary innovation is no longer a nice-to-have, but table stakes. If you want to earn trust and stay relevant, proof seems to be more important than ever.

Our Lens as an Investment Team: Tangible Over Trendy

Despite the pace of innovation, we approach this space with a healthy dose of skepticism. It’s easy to get swept up in the excitement of new modalities or viral trends, but we try to focus on what sticks, not just what spikes.

That lens informs how we think about the broader category. We see consumer health as a combination of behaviors, technologies and motivations. Our perspective is rooted in a few core beliefs:

- We prioritize behavioral reinforcement. In our experience, companies that embed into existing routines tend to have more staying power than those that require full lifestyle overhauls.

- We value visibility. Progress that can be seen, felt, or measured is often a better driver of adherence than abstract goals.

- We assess trust. In an age of information overload, trust can be scarce. Whether through credentialed experts, peer recommendations or proof of efficacy, consumers are often seeking validation.

The consumer health and self care companies we’ve backed that reflect these themes:

- Mirror (acquired by Lululemon): A rethinking of in-home fitness that aimed to merge function with form—and showed that connected fitness could feel aspirational.

- Ladder: Fitness infrastructure that leverages accountability and habit loops to help drive stickiness.

- Bliss Aesthetics: Built to capture the new demand emerging from body transformation trends. Focused on accessibility, transparency and personalization.

- Natural Cycles: A science-backed, non-hormonal birth control app that allows users to monitor fertility through daily temperature tracking and personalized insights.

- Boulevard: Vertical software solution for med spa owners to create more personalized self-care experiences.

- Quantune: A non-invasive glucose monitoring platform using laser spectrometry.

What’s Next for the Category?

In the near future, I think we’ll see greater interoperability between data sources (think wearables, diagnostics and apps) combined with AI-powered guidance. That could lead to more personalized, responsive recommendations across nutrition, fitness, sleep and stress management.

Even with all the hype and tech cycles, I think our core health needs haven’t really changed. At the end of the day, most people just want to feel good, age well and remove friction from staying healthy. New tools come and go, but what seems to stick are the solutions that make those fundamentals easier to achieve. Ultimately, I believe the real test of an enduring consumer health startup isn’t whether the science sounds fancy, but whether consumers stick with it—and whether, when they look in the mirror, they find themselves feeling better and realizing they got there more easily than they expected.

The post Inside the Consumer Health Renaissance: Navigating Personalized Wellness in a Shifting Landscape appeared first on Point72 Ventures.

]]>The post Defense Tech is at an Inflection Point – The Opportunities, Challenges and Innovations Shaping the Sector’s Future appeared first on Point72 Ventures.

]]>To the average observer, the most dramatic story of recent tech progress likely centers on generative AI’s seemingly breakneck evolution over the past several years. Yet behind the scenes and often beyond the view of the general population, we believe defense tech has been evolving just as rapidly. Now, several trends are converging, including geopolitical instability, an urgent need for more modern defense solutions, and maturing capabilities of dual-use technologies. As a result, governments are now reevaluating their priorities and looking beyond traditional large contractors for military and defense projects.

Together, these forces underscore our belief in the strategic importance of investing in solutions that enhance global stability and security. Emerging technologies are a key factor in the global power balance, and at Point72 Ventures, our view is that AI, autonomy, and software-first systems will redefine modern conflict with their prioritization of agility over mass and scale.

The Problem and the Opportunity

From 2020 to 2024, defense budgets increased by $146B in the United States and $480B globally. But we don’t think the pace of innovation has kept up. The defense industrial base was designed for a different era—one where 6-8 year timelines, monolithic programs, and hardware-first thinking were the typical norm. Today, our view is that’s not going to cut it. Recent conflicts have shown us that there’s an urgent need for new technologies including autonomous solutions, cybersecurity, electronic warfare, advanced manufacturing, energy and more.

Autonomous systems must operate in coordination, adapt on the fly, and reduce the need for human operators. Cyberspace is now a contested domain and, in our view, decision speed, the ability to evade surveillance, and offensive capability provide a clear advantage. And space has grown from a support layer to critical infrastructure.

At the same time, modern defense requires new ways to generate and store energy to move quickly and quietly through contested zones. This is where advanced manufacturing comes in.

We have seen that this is where startups shine because they can typically move fast, build modularly, and are increasingly staffed by people who’ve worked at the edge of both technology and mission. But for too long, we have seen them be shut out of meaningful defense spending.

Historically, less than 1% of total defense spending in the United States has been channeled into startups (venture investment in defense-tech startups reached approximately $3 billion in 2024, while the Department of Defense’s annual discretionary budget is around $850 billion). Now that seems to finally be shifting, with bipartisan support for strengthening industrial base capabilities and aligning commercial tech with national security goals. Other nations are following suit. All 32 NATO members have recently pledged to increase their defense and security-related spending to 5% of their GDP by 2035, some of which we anticipate could flow into startups.

To us, the opportunity is clear—and so is the urgency. To maintain deterrence, we believe we need to invest in the technologies that define the future, not the ones that won the past.

Why We Believe Specialized Support is Critical to Defense Tech Startup Success

Defense is not like other markets. Having the best technology will only get you so far. Success also hinges on understanding how the government buys, who the decision-makers are, and how to align with long-term programs of record. We often see startups win early R&D or pilot contracts, but struggle to transition into full-scale procurement. Navigating all of this requires a clear understanding of paths to acquisition, timing and budget windows.

The Department of Defense isn’t a single customer—it’s hundreds of stakeholders across services, commands, and acquisition offices. Each has different pain points, risk tolerances, and procurement approaches. Sales cycles often last multiple years, customers are often classified, and budget processes are often opaque. Our view is that specialized support helps startups identify the right customer and build for real demand.

Policy and timing matter, too, in an ecosystem where programs can shift quickly based on elections, budget cycles and evolving global threats. We don’t think startups in this sector can just track trends, but also must track policy developments, new executive orders, and upcoming budget authorizations so founders can time their moves correctly to have the best possible chance at success.

Another reality of defense tech: in our experience, talent and partnerships are hard to find. We have seen that startups need to tap into the expertise of those who understand both cutting-edge engineering and the unique, complex realities of the sector. Often, they need connections to advisors who have operated in classified environments, former military who know the on-the-ground realities and can validate and pressure-test product-market fit, and trusted lobbyists and legal experts who can help navigate security clearance and contracting.

Our Advantage: For Us, This is Personal

For our team at Point72 Ventures, being a dedicated partner to the next generation of defense tech companies is about more than investing. We care deeply about the sector because we’ve lived the mission firsthand with combined experience that includes the CIA, US Navy, Marine Corps, In-Q-Tel, BAE Systems, NATO Innovation Fund and Northrop Grumman. For the past five years, we’ve been investing in and supporting founders who we believe offer products that give those working across national security the tools they need to do their jobs effectively.

Our conviction as investors comes from the fact that many of us started out building and deploying systems, not just analyzing them. Now, we are able to evaluate defense startups like product managers to understand and form our opinions about what’s actually possible in the field. Our careers leading up to Point72 Ventures reflect in our networks, too. We’re fortunate to be part of a broader community of former users and operators who also answered the call to build for national security. These are relationships that have been built over many years, and often decades.

In short, we believe that succeeding in the defense tech industry requires more than building great products. We think it requires a deep understanding of government systems, timing and policy. Startups that can navigate this complexity stand to deliver transformational capabilities. But to do so, we believe they need investors and advisors who bring not just capital, but clarity, networks and real-world experience.

There’s much more work to be done in this sector and the potential for many more startups to be launched. To the talented and dedicated founders bold enough to build in one of the most difficult spaces out there, we’re excited to be your partners on that journey.

The post Defense Tech is at an Inflection Point – The Opportunities, Challenges and Innovations Shaping the Sector’s Future appeared first on Point72 Ventures.

]]>The post When AI Helps, Not Hurts, the Entertainment Ecosystem – Our Investment in Fever appeared first on Point72 Ventures.

]]>In December, I wrote about how media companies may view new technological advancements, especially AI, as a threat rather than an opportunity. And how they may have good reason to do so: from lawsuits over training data to platforms that undermine IP value, the entertainment industry has been put on the defensive.

But I also made the case that there’s another path: one where tech can help media companies monetize their content more effectively, and where AI is used to expand the value of IP, not exploit it.

I believe Fever is one of those companies.

Founded in 2014, Fever is a global live entertainment discovery platform that uses AI and behavioral data to help people find immersive, real-world experiences — with the goal of helping creators, producers, and IP holders fill more seats, earn more revenue, and reach more fans. Their tech stack is built around a data-driven engine that is designed not only to personalize recommendations for consumers, but also to help optimize pricing, forecast demand, and unlock incremental revenue.

I believe this approach is an example of the type of alignment between tech and media I discussed in my post in December. We do not view Fever as trying to outsmart the entertainment ecosystem; we believe it’s enabling it. Fever’s technology is specifically focused on discovery, distribution, and monetization and is set up to work with content owners, rather than around them.

For consumers, Fever is working to use AI to personalize event recommendations, helping them find new experiences beyond the usual concerts or Broadway blockbusters. For organizers, enhanced customer discovery tools could offer the chance to reach targeted audiences and optimize performance — two pain points we believe are persistent in the live events space.

But what makes Fever especially exciting to us is what they have been able to do with IP. Through their Fever Originals initiative, they partner with rights holders to develop exclusive, immersive events based on beloved properties from Bridgerton and Stranger Things to Van Gogh and Squid Game. These are more than just themed nights out; we believe they’re new ways to monetize content libraries, deepen fan engagement, and extend the life of creative work.

Image: Fever

In my opinion, the real bottleneck in today’s entertainment landscape isn’t production, it’s discovery. We already have access to more content than anyone could reasonably consume. As of 2023, it would take 36,667 hours or four years, two months, and eight days of nonstop viewing — to watch everything available on Netflix. For context, the average user only gets through about 2% of their Netflix library each year. Instead, I think the real challenge is distribution: how do you get the right content in front of the right audiences, at the right time? Fever’s model is targeting that directly, both through personalized recommendations and a broader tech-enabled approach to live event marketing.

At Point72 Private Investments, we believe in backing companies that are rethinking entertainment in ways that work with creators and content owners. Our early investments in Mirror as well as Range Media reflected that belief and our recent investment in Fever is a continuation of that strategy.

We see Fever as a critical piece of the next era of the experience economy — one where AI enables smarter, more personalized entertainment without compromising the creative integrity that makes it all worthwhile.

We’re excited to support Ignacio, Alex, Francisco, and the rest of the Fever team as they continue to build a platform that brings people closer to the experiences they love and helps creators and IP owners reach new audiences in meaningful ways.

The post When AI Helps, Not Hurts, the Entertainment Ecosystem – Our Investment in Fever appeared first on Point72 Ventures.

]]>The post Our Investment in CX2 appeared first on Point72 Ventures.

]]>We are proud to announce our lead investment in the Series A for CX2, a company we think is redefining electronic warfare (“EW”) with software-first systems built for adaptability, speed, and scale.

We believe that EW has long been a foundational – but often underrecognized – pillar of military operations. From jamming to spoofing to sensing, it has shaped conflicts for decades. In recent years, however, the domain has taken on new urgency. The rise of drones, software-defined threats, and spectrum-driven battlefields has made EW indispensable. Ukraine’s commander-in-chief recently named EW the country’s second-highest military priority, calling it “key to victory in the drone war”.

Despite this growing relevance, the U.S. has historically underinvested in EW. In his confirmation testimony, General Dan Caine said that the military has “lost some muscle memory” in the spectrum and that the military would have trouble defending itself against electronic attack from advanced adversaries. While rival nations have invested heavily in multi-domain spectrum capabilities, much of the U.S.’s EW stack remains tied to platforms which are outdated, large and exquisite like EA-18G-Growler and EC-130H-Compass Call. We believe these are powerful but expensive, hardware-bound systems that are slow to evolve. In response, the Department of Defense is taking a whole-of-force approach to EW modernization. For years, Army officials have said that EW “keeps [them] up at night” and the service aims to train every soldier in EW, while the Marine Corps and Air Force are pursuing parallel efforts to make EW more agile, expeditionary, and software-defined.

We believe modern EW must be distributed, tactical, adaptive, and software-native—and that is exactly what CX2 is building. The company’s AI-enabled platform is designed to autonomously detect, classify, and respond to RF threats at the edge. Its modular, hardware-agnostic architecture offers the potential for deployment across drones, vehicles, and other systems—enabling faster iteration, wider distribution, and significantly lower cost.

In our view, CX2’s four co-founders bring a rare mix of technical and operational depth: Nathan Mintz is a serial deep tech entrepreneur with national security expertise; Mark Trefgarne is a seasoned software founder who exited a company to Meta; Lee Thompson is a former SpaceX RF engineer; and Porter Smith is a former U.S. Army helicopter pilot and investor with firsthand experience as a former user.

EW is no longer niche—it’s foundational. And we believe CX2 is leading the way forward.

CX2 is but one portfolio company in which a ventures fund advised by Point72 Private Investments, LLC (“Point72 Ventures”) has invested. Additional examples of publicly announced investments are available on Point72 Ventures’ website.

The post Our Investment in CX2 appeared first on Point72 Ventures.

]]>The post Scaling our Commitment – Investing in Apex appeared first on Point72 Ventures.

]]>We are excited to announce our continued investment in Apex supporting their mission to revolutionize satellite bus manufacturing for the evolving space economy.

Spurred by the decline in launch costs, and the rise of proliferated constellations such as OneWeb and Project Kuiper, the demand for commercial satellites is robust. In fact, the General Accountability Office (GAO) estimates as many as 58,000 active satellites will be launched by the end of the decade. In the quest for more resilient space capabilities, the U.S. government is moving away from bespoke, expensive, long-lifespan satellites to more numerous, cheaper, and rapidly replaceable spacecraft. Additionally, expanded increases in U.S. Defense budgets over the next few years will likely increase national security demand for spacecraft, in our view. These tailwinds are not just limited to the United States, with other countries from Asia to South America pursuing their own sovereign space capabilities as barriers to do so come down.

Yet, the space industrial base is still largely oriented towards low-rate, exquisite satellites. The space supply chain struggles to keep pace with the demand of commercial and government customers as a result. In a high visibility example, the Space Development Agency recently announced it was delaying Tranche 1 of its proliferated constellation due to system readiness and supply chain issues. This is after the program saw one of its primes enter into litigation with a subcontractor over delays and reliability issues with supplied parts. This is not limited to the U.S. government. Commercial customers such as as Telesat, Viasat, and SES have all announced delays or reliability problems over the past three years because of supply chain issues.

Ian Cinnamon and Max Benassi built Apex from the ground-up to service the new space industry paradigm. Like the automakers of the Freedom’s Forge era, they are applying mass manufacturing techniques in an effort to deliver scale, efficiency, and reliability of their product. Apex’s configurable, standardized, buses are designed to limit bespoke engineering and leverage an extensible software layer to easily integrate with customers’ payloads. Their lineup includes spacecraft designed for geostationary, medium, and low earth orbit at significantly more affordable price points than traditional providers.

Following our investment in their Series B in 2024, we’re now proud to lead Apex’s Series C and work with Ian, Max, and the rest of the team as they build the supply chain to help support the new space industry.

Ad astra sine aspera.

The post Scaling our Commitment – Investing in Apex appeared first on Point72 Ventures.

]]>The post Our Investment in Luminance appeared first on Point72 Ventures.

]]>We’re excited to welcome Luminance, a London-based legal AI company, to our portfolio – joining our other founding teams with Cambridge roots including PolyAI, Glyphic, and Tunic Pay.

Our investment leads their $75M Series C round, fueling their growth as a leader in AI-powered legal automation and augmentation. Under the leadership of CEO Eleanor Lightbody, Luminance is working to transform how legal teams handle contracts, compliance, and workflows— and to deliver AI-driven innovations globally.

Based on discussions with a number of in-house legal professionals, we believe their teams are critical to sales and operational workflows, but they often grow slower than their counterparts in sales and operations. This gap has the potential to lead to bottlenecks, missed opportunities, and rising costs. With the demand for in-house legal services continuing to climb, 79% of legal departments expect increased demand in 2025, while 67% anticipate maintaining or shrinking their teams. As a result, we believe legal teams need new solutions to increase efficiency. AI adoption in legal workflows is gaining momentum, making workflow automation a top priority.

Luminance has designed an end-to-end legal AI platform that we believe is redefining contract management and analysis. The platform offers a tailored AI model, built by analyzing a company’s documents, contract rules, and clause playbooks, with the goal of empowering both legal and non-legal teams to more efficiently draft, review, and analyze documents with high accuracy. Luminance automates tasks like NDA reviews and contract analysis, with the goal of not only streamlining workflows but also surfacing critical insights, like flagging expiration dates, regulatory issues, and non-standard clauses before they become roadblocks. Luminance is also designed to integrate with platforms like DocuSign, Salesforce, and SharePoint. We believe its specialist AI has the potential to make navigating complex workflows as easy as having a conversation.

Our confidence in the AI-driven legal technology market remains strong. Nearly two years ago, we invested in Lexion, (since-exited), and we remain convinced that legal teams need solutions to navigate an increasingly complex and fast-paced landscape. Today, we’re excited to invest in Luminance, who we believe is an innovative leader in the space, with the potential to empower organizations to work smarter, faster, and more effectively.

We’re thrilled to support the Luminance team as they continue working to push the boundaries of what’s possible in legal AI. We look forward to supporting their vision, execution, and commitment to cutting-edge solutions in the years to come.

The post Our Investment in Luminance appeared first on Point72 Ventures.

]]>The post Doubling Down on Netradyne appeared first on Point72 Ventures.

]]>Point72 Private Investments is proud to be leading Netradyne’s $90M Series D round. We first partnered with Avneesh Agrawal and the Netradyne team back in 2018 when we invested in the Series B – today, we’re excited to double down on our investment as the company continues working to make commercial transportation around the world safer and more efficient.

Netradyne’s main product is Driver-i, an AI-powered, vision-based fleet safety platform designed to help companies manage their vehicles and enforce safe driving standards. Through continuous, real-time visibility into driver behavior, Driver-i rewards and incentivizes positive habits, and aims to decrease high-risk behavior such as distracted driving or speeding. To date, the platform has processed more than 18 billion miles of driving data and achieved 99% alert accuracy. As a result, Netradyne is building goodwill not only with fleet managers, but also with the drivers who use the platform every day.

Safety doesn’t just save lives, it is also good business – the Federal Motor Carrier Safety Administration (FMCSA) estimates that the average cost of a truck crash is ~$91,000, increasing to ~$200,000 if there’s an injury and $3.6 million if there’s a fatality. As fleet managers grapple with challenges like thin margins, a persistent driver shortage, high turnover, and rising insurance costs, driver safety and performance become existential operational considerations. We believe Driver-i has been able to consistently deliver material improvements in driver safety and operational efficiency for fleets of all sizes around the world.

When we wrote our first check into Netradyne back in 2018, we believed that video-based safety systems would become ubiquitous, and that Driver-i was best-in-class technology that would help establish Netradyne as the market leader in fleet safety. In the 6+ years since we made that bet, we’ve had the privilege of watching the Netradyne team deploy Driver-i into hundreds of thousands of commercial vehicles across thousands of customer fleets all over the world. There’s still much work to be done, but we are more excited now than we’ve ever been about Netradyne and its mission to make our roads safer.

We are thrilled to be continuing our support for Avneesh and the Netradyne team on the journey ahead.

The post Doubling Down on Netradyne appeared first on Point72 Ventures.

]]>The post Looking back on 2024: The AI playbook takes shape appeared first on Point72 Ventures.

]]>AI Founders’ Chicken-and-Egg Problem

Like many, we believe startups benefit from a moat. But creating one as a tech startup – especially an AI startup today – feels increasingly daunting. Investors and builders keen to find the next enduring businesses are increasingly looking to unique datasets as one potential moat. While some first-generation foundational model startups build upon public datasets (hence the name “wrappers”), the next wave of companies are seeking to amass and capitalize on their own novel datasets.

We believe the vertical application ideas leveraging proprietary datasets are the most likely to become long-term defensible businesses – but, how do founders acquire this data without an existing product, customer base, or go-to-market strategy? In this perspective, I’ll share my observations on how teams are navigating this paradox and offer illustrative examples as startups, founders and incumbents are collectively trying to write the next-generation’s playbook.

Propriety Datasets Can Help Startups Standout in a Crowd

We believe much of the low-hanging “software” fruit has been plucked. Either the software solution is increasingly commoditized and thus challenging the economics, and/or the incumbents possess an innovation advantage via resources, talent, historical data, existing customers, etc. Additionally, many pure-play software markets are becoming crowded markets – a Martech Map below for illustration:

{kind=link}

Source: chiefmartec.com

Be Opinionated, But Openminded

However, this can encourage early-stage founders to reinvent the typical startup playbook and for investors to be more progressive when evaluating potential business strategies. In our framework below, we charted hypothetical paths to a data moat – and potentially big businesses – by analyzing both their target business model and end markets over time. The arrows below represent five examples of hypothetical startups building novel datasets and pivoting the business upstream – seeking higher margins and/or Annual Contract Values (ACVs):

For example, the two lower arrows 1 and 2 represent hypothetical hardware startups that transformed into software-with-a-hardware-component businesses. Arrow 1 initially sold hardware to enterprise customers before building a consumer product, and arrow 2 consistently sold to government – both chasing higher margins with a business model evolution.

- Rethink Hardware Startups: While hardware development is capital-intensive and often lower margin, startups creating novel data through their hardware are attracting renewed investor interest.

In a quest to graduate beyond a great demo to a great product, we’re seeing some software-as-a-service businesses position themselves to be the next software leaders.

- Trojan-horse Services Businesses: While sometimes difficult to scale, services businesses can leverage their initial experience to inform product development and achieve a “good enough” offering at scale.

Additionally, we’re optimistic about founders reconsidering non-traditional venture markets, such as midmarket or government customers.

- Energized SMB Startups: Traditionally associated with lower contract values, we believe SMB-focused startups are attracting venture capital by building comprehensive end-to-end solutions instead of point solutions.

- Superpowering Local and Regional Governments: Aided by Defense Tech’s tailwinds, we read a trend of states, cities, municipalities, etc. considering tech-forward solutions to improve efficiency and/or increase revenue.

Finally, these new datasets have the potential to be steadily improved to help that company stay ahead of competitors. In our view, the unique insights from this data can then open up more opportunities and use cases, making the data a valuable asset.

Enhancing “Better, Faster, Cheaper” for the AI Era

When building a data moat, we believe it’s crucial to determine whether you’re aiming for depth or breadth:

- Deep (Vertical Focus): Are you striving to become the default solution for a specific niche?

- Wide (Horizontal Focus): Are you aiming to solve a similar problem across various sectors and industries?

Next, you might consider some of the following questions:

- Quality: Are you improving the collection or utility of data?

- Collection: Are you building proprietary technology to enhance data quality? Quantune’s advancements in optics and photonics technology exemplify this approach, aiming to create an accessible instrument without compromising data quality.1

- Utility: Are you breaking down data silos? For example, Glyphic’s AI sales copilot aims to leverage customer conversations to empower data-driven decisions across departments. 1

- Time: Are you creating new markets, growing existing ones, or accelerating adoption?

- Ephemeral: Is the value of your data short-lived, similar to live sports? Blackshark’s efficient 3D mapping for change detection illustrates this concept. 1

- Perpetual: Are you generating valuable data byproducts? Netradyne’s fleet safety technology also enables fleet management and compliance solutions, demonstrates this principal. 1

- Pace: Are you accelerating your customers’ ability to act based on data insights? PolyAI’s customer-led voice assistants, deployable in weeks, showcase this rapid value delivery. 1

By identifying the desired data asset, we believe founding teams can more effectively shape their early product and choose initial partners or customers to help build that specific dataset.

Selling Budget Protection or Convenience Bliss?

One challenge many founders may face is acquiring those initial design partners or customers who will kickstart the data flywheel needed to attract future customers. To overcome this paradox, we believe you need a “wedge product” that delivers immediate value, establishes early relationships, and encourages customer retention.

Two common approaches to building a successful wedge product include:

- Sell on Budget: Can you offer a more affordable solution that provides immediate value?

- Sell on Convenience: Can you streamline a process to save customers time and hassle?

This initial offering may provide access to valuable data or generate proprietary data as a byproduct. From there, we advise founders to focus on creating a virtuous loop:

- More customers lead to…

- More insights, which enables…

- More value delivery, resulting in…

- More customers, continuing the cycle and reinforcing your data moat.

As your data asset grows, we believe you should begin introducing features that leverage the asset to push insights or actions. This old-school transition is exemplified by companies like Instagram, which evolved from a photo editing app to a data-driven social media platform.

NRR is the new ARR

Retaining your customers is paramount, as we believe many investors are increasingly prioritizing Net Revenue Retention (NRR) over net new Annual Recurring Revenue (ARR). This “stickiness” may reveal enterprises transitioning from their innovation budgets to core spend, and ultimately validating your product as “good enough” not just “good.” With a sharp focus on retention, startups can expand within existing accounts and leverage a repeatable onboarding process. At the same time, these startups can increase their margin profile by introducing higher-margin, software-like features powered by their growing data assets.

Navigating Common Pitfalls

Building a successful AI data moat is not without its challenges, and the below are some common pitfalls that we’ve observed:

- Over customization: Excessive customization for early customers can inadvertently lead to building a services business that lacks scalability.

- Targeting the Wrong Customers: Catering to the wrong customer profile can trap startups in local maxima, sacrificing the pursuit of a larger market opportunity.

- Rigid Ideal Customer Profile: Sticking too rigidly to an ideal customer profile can blindside startups to unforeseen opportunities.

Talk Data to Us!

Ultimately, we believe that regardless of your starting point, strategizing how you can turn your initial dataset into a novel asset will be time well spent. While you can’t predict every step amid this quickly changing landscape, you can think early and often about your data moat. By prioritizing data acquisition and taking a disciplined approach to product development and customer selection, we believe you can build a wedge product that sets your flywheel in motion. If you’re a founder building in the space, a researcher, or an operator, we’d love to hear from you.

- Selected portfolio companies. For a full list of our portfolio, please visit Portfolio – Point72 Ventures

The post Looking back on 2024: The AI playbook takes shape appeared first on Point72 Ventures.

]]>The post How AI media startups can help solve existential issues for the industry and artists appeared first on Point72 Ventures.

]]>I encounter a surprising number of AI media startups that offer tools whose use I cannot intuit; whose features make me wonder, “Who would actually want to do this?” And whose models seem to have been built or trained without considering intellectual property (IP) law.

Perhaps there’s an advantage to entering an industry with no prior knowledge. But is it a good idea? In media? Take Napster. Napster disrupted music. But the music labels sued it and forced it to shut down. I believe history shows the music and entertainment industry is unkind to startups that ignore copyright: The value chain is complicated and full of litigious players and established rules.

This is relevant because we have entered an era where AI is good enough to produce believable images and art—where you no longer have to be trained as an artist to create remarkable drawings or songs—and I expect there will soon be a lot of this content. Especially since this next wave of startups can build upon already strong foundational models that are now two years old.

In this article, I explore some of our observations and the enduring media dynamics I believe some generative AI startups overlook. It’s based on our thematic research plus conversations with nearly 80 people building in this industry, investing in it, or directly impacted by it.

Don’t build a legally dubious business

Naivete may free you to innovate, but it may also expose you to age-old risks. Where major labels attacked Napster, they eventually welcomed Spotify, which played by the rules and paid them royalties. Spotify respected copyright. If you’re a founder working in this industry, take the time to learn it. There are layers of financiers and administrators, music labels and movie studios, producers and distributors, each with their own economic interests and legal teams. After our work researching this space, my conclusion is that these players are willing to work with startups, but on their own terms.

Don’t make the mistake of ignoring them and training on datasets you do not have permission to use. IP owners are watching and many are taking legal action. For example:

- Suno and Udio are being sued by major labels for copyright infringement.

- Pocketpair Inc. is being sued by Nintendo for patent infringement.

- OpenAI is being sued by the New York Times for infringement.

- Stability AI is being sued by Getty over watermarked images.

- Anthropic is being sued by Universal Music Group over song lyrics.

- Perplexity is being sued by News Corp for copyright violations.

Those lawsuits are compelling AI companies to pay publishers for access to their content. To me, these lawsuits suggest that the days of unregulated training data are coming to an end. And while we’ve spoken with IP attorneys who don’t think there will be significant legal action to shut down companies like OpenAI, we do believe startups should put aside some of their capital to fight legal cases as they arise.

But consider this. What if instead of running these risks, your startup embraced IP law? Some are building technology to do that. For example, NEX, Raive, and Bria AI are working to build foundation models that allow application developers and IP holders to know precisely what was in the training set. That could greatly reduce the risk and give IP holders the opportunity and incentive to participate, like the Council of Fashion Designers of America, which has partnered with Bria AI.

All to say, we believe it’s best to build a business where the model respects the existing ecosystem.

Try to solve a real problem

I recently came across an AI video generation app where you can type text to generate a several-seconds-long video. The tech is computationally expensive so it can’t actually create more than that. And the output is typically not very watchable. In which case, what is the point? This is one place I believe some AI startups go wrong—they don’t address an existing problem.

There are plenty of existing media problems to solve. As just one example, AI could help IP owners instead of exploiting them. As an artist myself, I take offense to infringement given the effort and dedication that goes into putting your work out there, just to have others use it without permission. Today many artists struggle to prevent others from infringing upon their copyright, and the companies that represent those artists sometimes use software to monitor the internet and social media to, say, block YouTubers from using song clips. But they are finding it harder to protect their work when more creators are remixing and speeding up their songs.

Could your AI tech startup safely empower remixers to respect artists’ rights? To allow for widespread, IP-safe sharing and reuse? Some music labels may be coming around to the idea. “Rights holders understand that this process is inevitable, and it’s one of the best ways to bring new life to tracks,” Meng Ru Kuok, CEO of music technology company BandLab, told Billboard.

Or consider how expensive intellectual property is for artists to create, and what a short life it can have. Artists or labels make money when their music is streamed, but there’s often a drop-off after launch. What if that wasn’t the case? What if an AI platform allowed fans to remix songs with the artist’s permission to spark a new generation of fandom, as has happened for the band Fleetwood Mac on TikTok? (The AI startup Hook — one of our portfolio companies — is focused on creating this platform.)

Or consider smaller artists without the legal resources necessary to license their music. Could startups help them license to local radio stations or TV channels? It’d be similar to how publishers like The Atlantic strike deals with OpenAI, but for everyone else. Two companies, Created by Humans and Human Native AI, are working on such licensing platforms.

Or what about using IP to help with generative AI’s engagement problem? ChatGPT famously reached 100 million users, making it the fastest-growing consumer application in history, but then usage fell. We read this initial spike as evidence consumers are excited, but now these companies must give them a reason to stay. Perhaps media crossovers could sustain this demand. Coca-Cola, for one, opened its archives to allow creators to remix images with DALL-E. The so-called “creator economy” is expected to reach $500 billion by 2027. How can you help those creators monetize while working with existing IP holders?

I believe founders need to think critically about the problem they’re solving. Look at big consumer businesses. They tend to be big because people use them. How are you using technology to allow people to do things they previously couldn’t, and would pay to?

Find a way to differentiate

Let’s say you work at a media-related startup that has built a legally upstanding business that addresses a real problem. If it’s a real problem, there are likely competitors. How do you differentiate? I believe it helps to deeply understand what the media and entertainment industry is facing today to solve those problems in a noteworthy way.

To me, the great challenge in media today is not on the supply side. Artists and media companies want to grow, but they are constrained by the ever-finite sum of consumer attention. Box office visits are down marginally this year. The streaming wars are tapering off. There’s too much competition for too few eyeballs.

Yet I see many AI companies still trying to help creators create more. We can now create far more content than anyone can possibly watch. Streaming consumers aren’t looking for infinite titles—their attention is finite and they’re looking for shows and movies they enjoy, which they say is nearly as important to them as cost. What makes Netflix and Max (formerly HBO Max) great, in my opinion, is the quality of their content. So how can AI startups solve that problem? How can they help build audiences and bring more viewers for more time?

The demand/distribution side is also where I feel the money is made—the value is captured at the connection to customers. For example, Spotify doesn’t make music, and Netflix only makes some of its content. How might your startup open new channels to allow IP owners to distribute their works? I think there is still room for new players. For instance, Webtoon, which offers smartphone-native comics, just went public at $2 billion.

Source: Spotify (as of 12/09/24), Riverside FM, Netflix (as of 12/09/24), A24, YouTube (as of 12/09/24), ProTools, SnapChat (as of 12/09/24), Shutterstock (as of 12/09/24)

Finally, don’t discount the power of fandom. Many artists and creators are worried about AI’s power to create, but I personally believe people are invested in these artists because they are people. Would someone listen to AI Drake and get just as much value? Perhaps. But what many people seem to really care about is Drake’s beef with Kendrick Lamar. Artificial music doesn’t replace real drama.

So how can AI help those artists do more things that are truer to them? Perhaps AI can help them with writer’s block, remaster old footage, or finish an incomplete song as Paul McCartney did with John Lennon’s work. Platforms are flooded with content. If fandom matters, what are the bottlenecks to those fans enjoying the artist even more?

Media companies want to work with AI startups—on their own terms

I believe there is great potential for generative AI startups in media and entertainment. Especially since the foundation models are so good, creators can build on top of them. (Including new, IP-protective ones.) The question is, will they build in a way that plays by the industry’s rules and uses those forces to their own advantage? Or will they fight like Napster and potentially go down in a blaze of legal action?

I’m optimistic and excited to see what emerges. If you’re a founder building in this space, or a researcher or investor, I’d love to hear from you.

The post How AI media startups can help solve existential issues for the industry and artists appeared first on Point72 Ventures.

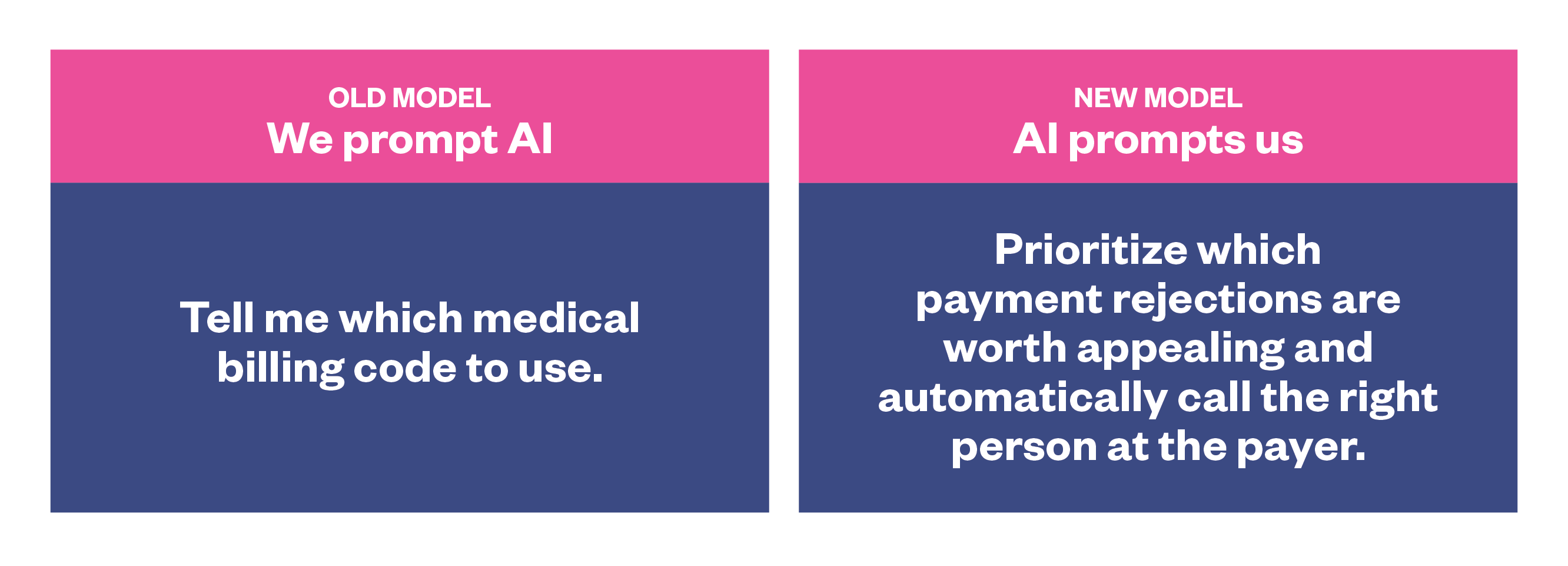

]]>The post Clunky copilot or benevolent boss? Why I believe AI should prompt us appeared first on Point72 Ventures.

]]>Consider how much time predictive typing on your phone or in email saves you. Perhaps one minute per day? If so, those savings don’t exactly reduce our work to the 15-hour work week John Maynard Keynes predicted in the 1930s. In fact, one study of 37,000 people found predictive typing actually slowed them down. But that’s the sort of AI available to the mass market these days and there is a lesson in that.

I believe predictive typing is representative of the way many companies are applying AI—in ways that feel obvious but ultimately don’t increase productivity. I personally don’t think we need an AI to finish our sentences. And we shouldn’t need to prompt an AI to write us something. Instead, I think AIs should be prompting us.

It’s my belief that the right tool with access to the full repository of our work information can draw upon enough context to tell us what to prioritize. Rather than an AI copilot, it’d be a chief of staff that knows enough to set the agenda.

Perhaps this sounds counterintuitive or dystopian, but let’s explore what it would look like applied to four common use cases where, in my observation, AI copilots haven’t yet made a meaningful productivity difference.

Most jobs aren’t actually that easy to automate

Let’s define what we mean by AI: software that uses algorithms to simulate human intelligence by reasoning, drawing conclusions, applying judgment, and possibly, acting on the result. The current generation of models perform best where the success criteria are repetitive and clearly defined, such as making a diagnosis, producing an image, or answering a question.

When it comes to divergent, nonlinear thinking, skilled humans still outperform AI on a range of tasks—like most jobs require. Because while a majority of workers do some repetitive tasks, my sense is that most jobs are actually full of heterogeneous tasks. It’s part of what makes work interesting. There may be some areas where automation can completely eliminate rote, repetitive jobs, but I observe that software as a service (SaaS) has largely done that or made serious inroads. The big opportunities in AI, I believe, will not necessarily all come from further process automation.

The big opportunities in AI, I believe, will not necessarily all come from further process automation.

At least some Wall Street analysts are reporting that only one publicly traded software company has reported revenue/profit gains as a result of using gen AI. To me, it’s worth asking whether copiloting really drives productivity gains. AI startups also appear to have lower gross margins than other software startups: that computation is expensive, especially compared to the output.

Yes, there are many studies about jobs “exposed to AI” on the assumption the gains will come from process automation. But I find most literature on this flawed because it confuses potential with probability, in the same way people in the 1950s felt flying cars were imminent because they were possible. Mind you, that primary “replacement” study was produced by OpenAI, which sells AI software. And Pew Research’s definition of “job exposure” is based on conjecture and thought experiments, not actual tests.

So where’s the AI opportunity? Consider what actually restricts worker productivity: I think it’s that people don’t know what action to take next. They’re blocked when their instructions are vague or abstract, or where they’d have to sift through an unrealistic volume of information to prioritize their day.

What if instead of AI saving people one minute per day writing emails, it saved them one hour in organizing their materials for a meeting? Or saved them two hours by canceling meetings that lack an agenda? Or told them the optimal way to spend their day?

AI may be able to help us get clear on the most valuable activities so we can focus on just those. I have observed that this is difficult for people because while enterprises are awash with information, a human can only access and weigh so much. Brains have limits. Our working memory is just seven numbers in a string or 3-5 essential items, and the prevailing theory is we can only maintain 150 close relationships.

Machines do not face these precise limits. This is not to bash the brain. It’s the result of 500 million years of experimentation. But AI by comparison has a vastly larger active memory and capacity for more concurrent connections. It doesn’t just review some Slack messages. It can access all of them, all of the time, for every decision.

So why don’t I see more AI startups taking the chief of staff approach, where the AI uses all that data to make decisions and prompt us?

Perhaps startups find the copilot model appealing because it requires less context. Or perhaps these startups are following in the well-worn groove of some software applications that came before, which aimed to solve task management issues. But imagine the chief of staff model applied to these use cases, where instead of you filling in the software, the software fills in itself. You might go from digitally recording a meeting you booked to the AI booking your meetings, declining requests, and also making cancellable dinner reservations.

One of the great benefits I see to the chief of staff model is it could attune itself to you. If you correct it, I believe it would be able to learn your preferences just as a person would. I am excited about the idea of a tool that taps into AI’s potential to be a learning machine, realizing that you prefer new business calls in the morning and to not have meetings the day after a red-eye flight.

I can see this applying to industries such as the following hypothetical examples:

- Medical billing—In the copilot model, AI can help workers input medical reimbursement codes marginally faster (the predictive typing approach). But in the chief of staff model, I believe it could aim to make people more productive. It could scan all those files and say, “Here are the 37 billings that are the most valuable, do those first. Reject that dental visit, don’t reject the cosmetics claim,” and so on.

- Legal issues—AI drafting or reusing clauses is an okay use case, though only slightly faster than without AI because a human must still verify the work. I believe AI applied to helping you identify legal risks could generate much more value. For example, “These 17 leases will auto-renew, do you want that? And this contract you signed three years ago has a pricing uplift charge you should contest. And this contract has a typo that substantially alters the meaning of this provision, and you should correct it.”

- Customer success—I believe an AI chief of staff could use a wide variety of data (emails, tickets, app telemetry, phone calls, and more) to pinpoint what’s working and what’s not in a customer relationship. It could possibly observe what works across similar accounts based on the geography, product features, and champion profile to suggest a next-best action to that account manager. This approach could theoretically transform a one-to-many customer success strategy into a many-to-many approach for all accounts—something that today is very difficult at scale.

- Product management and user research—I believe AI could simulate user behavior at scale to predict how users will interact with (or break) software. These insights might proactively guide engineers towards additional features that would increase engagement, flag bugs, or safeguard against bad behavior. It would be something of a virtual product manager or chief of staff for engineers.

How does this work practically?

I think the chief of staff play may best be tested as an enterprise use case. There, people usually aren’t fully deciding on how to spend their time, and the data is multitudinous and reasonably well-structured in record-of-work software. If organizations are setting clear goals for their people but the prioritization is nebulous, I believe an AI chief of staff could work its magic.

This is something I’m thinking about a lot as an investor. And also, as an individual who interacts with predictive typing in my email where I suspect it slows me down. I believe AI can do much more for us. If you’re a founder or researcher in this space who wants to talk, I’d welcome the conversation.

The post Clunky copilot or benevolent boss? Why I believe AI should prompt us appeared first on Point72 Ventures.

]]>The post Where conflicts are determined by logistics, startups are innovating to win appeared first on Point72 Ventures.

]]>When Russia invaded Ukraine in 2022, its massive tank column reached the capital Kyiv in less than one week—then stalled just 30km outside. After days of waiting for resupply, those soldiers retreated and with them went Russia’s hopes for a sudden coup.

Military experts have noted this isn’t a one-off anecdote—it can be emblematic of how real conflicts transpire. Though they aren’t frequently mentioned, logistics and materiel often play important roles. During the 2000s conflicts in the Middle East, approximately 52% of casualties occurred from hostile attacks during resupply missions, even with total ground and air dominance. Logistics may not always decide conflicts, but they are a key factor, because at the end of the day, “all our operations are underwritten by logistics,” as the Secretary of the Air Force Frank Kendall has said.

And now, logistics are growing more difficult and future conflicts could occur in more inhospitable regions, against more advanced adversaries using technology to disrupt supply lines from afar. This is why the U.S. Department of Defense (DoD) is actively identifying its innovation gaps in logistics, many of which we believe startups are best positioned to fill.

Logistics are growing more difficult