Featured Research

Macroeconomic Insights: LATAM Fights an Oil Shock

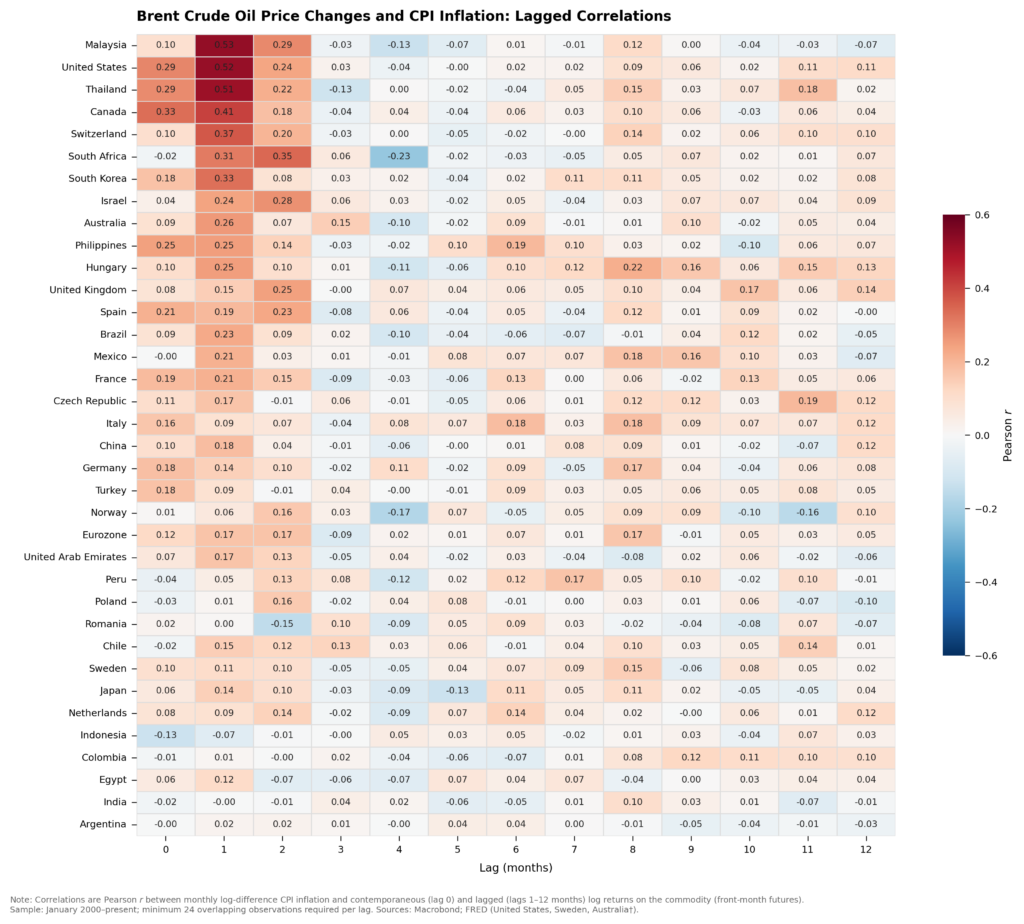

In an earlier post, we explored the lagged correlations between Brent crude oil price changes and CPI (Figure 1). Here, we see that for many LATAM countries pass-through is weaker and relatively slower than countries like the U.S. and South Korea. Figure 1 The...

Macroeconomic Insights: LATAM Fights an Oil Shock

In an earlier post, we explored the lagged correlations between Brent crude oil price changes and CPI (Figure 1). Here, we see that for many LATAM countries pass-through is weaker and relatively slower than countries like the U.S. and South Korea.

Figure 1

The inflation impact of an oil shock in Latin America can be understood by considering three layers of transmission:

- Exposure – whether a country is a net importer and how heavily fuel weighs in the CPI basket

- Extent of intervention – whether a country decides to leverage subsidies or administrative price controls or whether they already have automatic stabilizers

- Cross-elasticities – second-round responses to food, transport, FX, and domestic supply disruptions

Most governments in the region are actively smoothing pass-through, so the immediate inflation effect is being shaped more by administrative choices than by the external shock itself. But that insulation is uneven. At one end, Mexico and Brazil remain relatively buffered. At the other, Peru is absorbing a largely unfiltered shock. In between, Colombia is actively offsetting global price pressure, Chile faces a policy-driven regime shift risk, and Argentina is allowing pass-through, but gradually. In the following sections, we go into cross-country pass-through in greater detail.

Mexico — Most Insulated

Mexico remains the most insulated economy in the region. President Sheinbaum has capped retail gasoline prices at MXN 24/litre, while the IEPS excise tax continues to operate as an automatic stabiliser, compressing as international prices rise. Together, these mechanisms sharply reduce the transmission of Brent into consumer fuel prices.

The constraint is fiscal. The longer oil prices stay elevated, the more IEPS revenue is sacrificed, raising the eventual probability of adjustment.

Brazil — Contained, but with a Diesel Tail Risk

Brazil has also contained near-term pass-through. Petrobras has signaled that it will not fully transmit the shock to domestic prices, and the government is moving to eliminate the PIS/Cofins levy on diesel imports. On the gasoline side, the increase in the ethanol blend to 30% provides an additional cushion.

The main vulnerability is diesel. Brazil still imports roughly a quarter of its diesel needs, leaving part of the economy exposed to higher global prices. At the same time, rising fertiliser costs, particularly urea, create a secondary channel into food inflation if the shock persists.

Colombia — Offsetting the Shock

To read the rest, visit our latest Substack post, here.

Research Archive

Macroeconomic Insights: LATAM Fights an Oil Shock

In an earlier post, we explored the lagged correlations between Brent crude oil price changes and CPI (Figure 1). Here, we see that for many LATAM countries pass-through is...

Macroeconomic Insights: Airfares Take Off as Iran Conflict Continues

The war in Iran has persisted far longer than anticipated, driving sustained increases in global commodity prices. These pressures are now filtering into downstream products...

Macroeconomics Insights: Oil Prices Up, Will Food Prices Follow?

Over the past three weeks, the escalation of conflict in the Middle East has coincided with a clear increase in Brent crude prices, reinforcing the expectation of near-term...

Macroeconomic Insights: Iran’s Oil Shock Fuels Inflation

It’s been more than 2 weeks since the US-Israel joint combat mission against Iran began and the conflict doesn’t look like its going to end any time soon. Iran is doing...

Macroeconomic Insights: Energy Price Pass-Through to Inflation

Brent crude has surged from ~$70 to above $100 following the US-Israeli strikes on Iran and the near-closure of the Strait of Hormuz (Figure 1). Dutch TTF natural gas has jumped...

Macroeconomic Insights: Strait of Hormuz and the Inflation Shock Markets Are Repricing

The US-Israel strike on Iran has pushed Middle East risk back to the center of global pricing. Crude has firmed into the low 70s while European gas prices spiked, and gold has...

Macroeconomic Insights: Trump’s Tariff War – The Sequel

On Feb 20, 2026, the Supreme Court ruled 6–3 (Learning Resources, Inc. v. Trump) that the International Emergency Economic Powers Act (IEEPA) does not authorize the U.S....

Macroeconomic Insights: Gold’s New Inflation Playbook

Gold has stopped trading as a clean derivative of US real yields and now reflects a broader external pricing regime. Since 2022, the real-yield anchor has weakened, gold has...

TradeTech FX USA 2026

Over recent years, the finance community in Miami has grown, given that a number of hedge funds have opened up large offices there. Every February, the FX community from New...

Macroeconomic Insights: India CPI – Basket Reweighting Explained

India's National Statistical Office launched a new Consumer Price Index series on February 12, 2026, shifting the base year from 2012 to 2024 and overhauling the basket...

Macroeconomic Insights: UK CPI — Assessing the Renters’ Rights Act 2025

Executive Summary The Renters' Rights Act received Royal Assent on 27 October 2025. Council investigatory powers commenced on 27 December 2025, and the main rent-setting...

Macroeconomic Insights: South Africa CPI – When Currency Strength Meets Energy Vulnerability

After trending downward through most of 2025 alongside rand appreciation and falling oil prices, Turnleaf’s 12 month inflation forecast for South Africa is now pointing at rising...

Macroeconomic Insights: Colombia CPI: The Minimum Wage Shock

Colombia’s 12-month inflation outlook for 2026 has been revised higher. We now expect inflation to hit up to 6.7%YoY by the end of the year (Figure 1). This is a clear break from...

Macroeconomic Insights: Expect the Unexpected

Mark Carney at Davos, January 20, 2026 "For decades, countries like Canada prospered under what we called the rules-based international order. We joined its institutions, we...

Macroeconomic Insights: Eurozone CPI — “Sweater Weather” Is Repricing Energy Risk

Energy markets have moved back to the foreground as a near-term driver of Eurozone headline inflation. Colder January temperatures lifted heating and power demand into a winter...